Your Shopify store is doing $50K a month. Orders are flowing in. Your P&L shows a healthy profit. And yet, you’re scrambling to pay your next supplier invoice.

What’s in This Article

Sound familiar? You’re not alone. Research shows that over 70% of ecommerce businesses run into cash flow problems even when they’re technically profitable. The reason is brutally simple: profit is an accounting concept, but cash is what pays your bills. And in ecommerce, there’s almost always a gap between when you spend money and when you receive it.

The brands that scale past the $1M mark aren’t the ones with the best products or the biggest ad budgets. They’re the ones that figured out how to manage the timing of their cash. They know exactly when money is coming in, when it’s going out, and how to make sure those two things never collide in the wrong order.

This guide breaks down the entire cash flow system for ecommerce, from understanding your cash conversion cycle to building a weekly forecasting rhythm that means you never get caught short again.

Why Profitable Stores Still Run Out of Cash

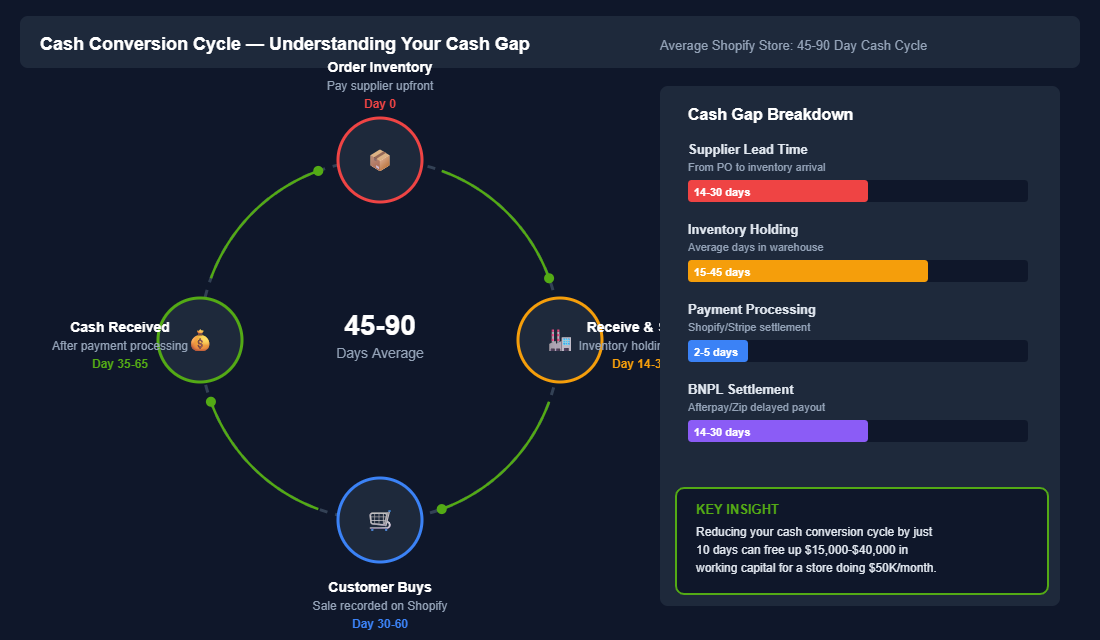

Here’s the scenario that catches most store owners off guard. You place a $25,000 inventory order in January. Your supplier wants payment in 14 days. That stock arrives in your warehouse three weeks later, sits for another two to four weeks before it sells, then Shopify batches your payout over 2-5 business days. If the customer paid via Afterpay or Zip, you might wait another 14-30 days for settlement.

Add it up and you’ve got a 45-90 day gap between spending the money and getting it back. During that window, your bank account is haemorrhaging, even though every single one of those orders is profitable on paper.

This is what accountants call the cash conversion cycle, the number of days between paying for inventory and collecting cash from sales. According to Barclays research, 35% of online retailers experienced cash flow difficulties even while reporting revenue growth. The faster your store grows, the worse this problem compounds, because growth means bigger inventory orders, higher ad spend, and more working capital locked up in the pipeline.

The average ecommerce store carries inventory representing 40-60% of total assets. That’s a massive chunk of your capital sitting on shelves instead of working for you. And with carrying costs running at 20-30% of inventory value annually, every dollar of unsold stock is actively costing you money.

Understanding Your Cash Conversion Cycle

Before you can fix your cash flow, you need to measure it. Your cash conversion cycle (CCC) is made up of three components, and each one is a lever you can pull.

Days Inventory Outstanding (DIO), how many days your stock sits before it sells. For most Shopify stores, this ranges from 30-60 days. Top performers keep it under 30 by running tighter assortments and using demand forecasting. If your turnover ratio sits between 4-6x per year, you’re in healthy territory. The best operators push above 8x.

Days Sales Outstanding (DSO), how long after a sale until you actually have the cash. For direct Shopify sales via credit card, this is 2-5 days. But if a meaningful portion of your revenue comes through buy-now-pay-later providers like Afterpay, Klarna, or Zip, your effective DSO stretches to 14-30 days. Marketplace sales (Amazon, eBay) add another layer of delay with their own settlement cycles.

Days Payable Outstanding (DPO), how long you have to pay your suppliers. This is the one lever that works in your favour. If your supplier gives you Net 30 terms, that’s 30 days of free float. Net 60 is even better. Many Australian ecommerce brands start on prepayment or Net 14 and never think to negotiate, that’s money left on the table.

The formula is simple: CCC = DIO + DSO – DPO. If your inventory sits for 45 days, your payment processing takes 5 days, and your supplier gives you Net 30 terms, your CCC is 45 + 5 – 30 = 20 days. That means for every dollar of daily sales, you need 20 days’ worth of working capital to keep the engine running. Reduce that number by even 10 days and you could free up $15,000-$40,000 in working capital for a store turning over $50K a month.

The Five Cash Drains Every Shopify Store Needs to Plug

Once you understand the cycle, you can start identifying where cash is leaking. Here are the five biggest offenders we see in ecommerce businesses doing $30K-$300K per month.

1. Over-ordering inventory “just in case.” Fear of stockouts drives most store owners to order more than they need. The result? 42% of small businesses struggle with overstocking. Every extra unit sitting in your warehouse is cash you can’t use for ads, team, or growth. The fix: order based on sell-through data, not gut feel. Use your Shopify analytics to calculate your actual weekly sell-through rate per SKU, then order to cover your lead time plus a small safety buffer, not three months of hopeful projections.

2. Ignoring the ad-spend-to-cash-collection gap. You spend $500 a day on Meta Ads. Meta bills your credit card weekly. The orders those ads generate take 3-5 days to settle through Shopify Payments. If you’re scaling aggressively, you can easily have $15,000-$20,000 in ad spend hitting your card before the resulting revenue arrives. This is the gap that catches fast-growing brands off guard, especially during peak periods like Black Friday when spend doubles but settlement timing doesn’t speed up.

3. Paying suppliers too early. If your supplier offers Net 30 and you’re paying on Day 7, you’re giving up 23 days of free float. That’s real money. A $20,000 order paid 23 days early at a 6% cost of capital means you’re effectively paying an extra $75 every time, and that adds up across dozens of orders per year. Use the full payment window your supplier gives you. Better yet, negotiate for longer terms.

4. Not accounting for GST timing. This is an Australian-specific trap that catches many store owners. You collect GST on every sale, but it’s not your money, it’s the ATO’s. If you’re spending that GST float on inventory or ads without setting it aside, you’re building a hole that gets deeper every quarter. The BAS payment hits and suddenly you need $15,000-$30,000 that you thought was working capital.

5. Seasonal inventory builds without cash reserves. If your business peaks over Christmas, you’re probably placing your biggest inventory orders in September-October. That’s three months before peak revenue. Without a cash reserve strategy, you’ll either need to take on debt, miss the buying window, or sell equity. None of those are great options when a simple cash reserve plan could have solved it.

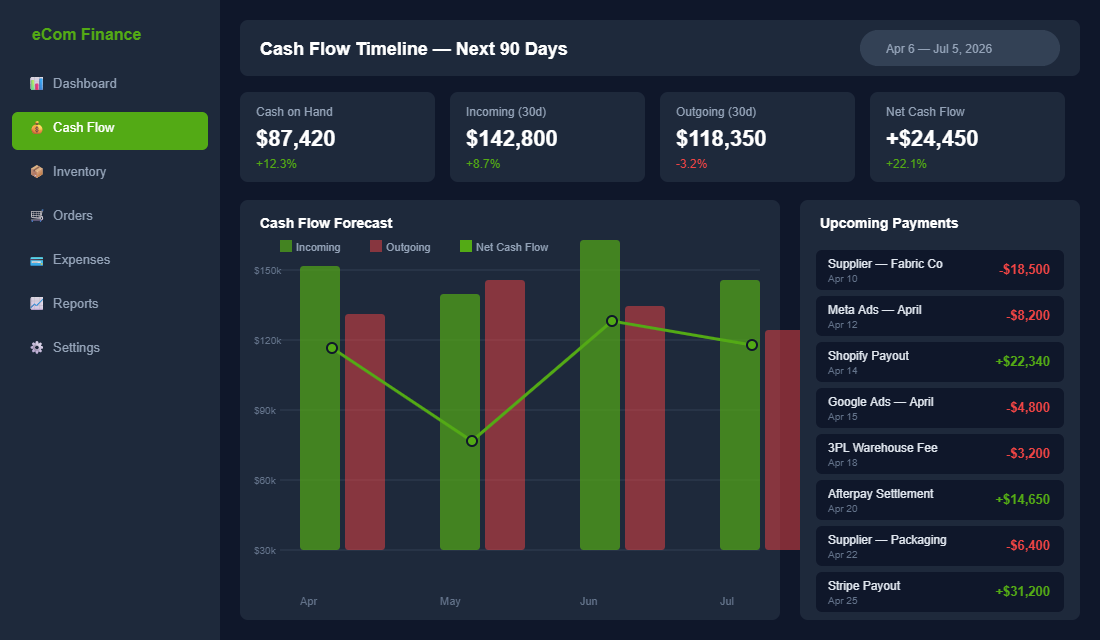

Building a 13-Week Cash Flow Forecast

The most successful ecommerce brands treat cash flow forecasting with the same rigour as their marketing analytics. They don’t check it monthly when the accountant sends a report, they look at it weekly.

A 13-week rolling forecast is the gold standard. It’s long enough to see problems coming (like that big supplier payment in week 8) but short enough to be accurate. Here’s how to build one.

Start with your opening cash balance. Log into your bank account and record what you have right now. Not your Shopify balance, not your accounts receivable, your actual bank balance.

Map your expected inflows week by week. Look at your trailing 4-week revenue average on Shopify, then adjust for seasonality and any planned promotions. Be conservative. If you averaged $52,000 in revenue last month, don’t project $60,000 this month unless you have a specific reason. Factor in the settlement delay, this week’s sales land in your bank next week.

Map every known outflow. This includes supplier payments (check your POs and payment terms), ad spend (your daily budget × 7), payroll, rent, software subscriptions, 3PL fees, shipping costs, and your quarterly BAS. Most store owners forget at least two or three recurring expenses the first time they do this. Go through your bank statement line by line for the last 90 days to make sure you catch everything.

Calculate your weekly net position. Opening balance + inflows – outflows = closing balance. That closing balance becomes next week’s opening balance. If you see any week where your closing balance drops below your minimum cash buffer (we recommend keeping at least 4 weeks of fixed costs in reserve), that’s your warning signal to take action.

Update this forecast every Monday morning. It takes 20 minutes once you have the template set up, and it’s the single highest-ROI financial habit you can build. You’ll spot problems 6-8 weeks before they become crises, which gives you time to pull levers instead of scrambling.

Seven Tactics to Shorten Your Cash Cycle

Once you can see your cash flow clearly, here are the specific moves that make the biggest difference.

Negotiate longer supplier terms. This is the single biggest lever most brands never pull. If you’ve been ordering consistently for 6+ months, you have leverage. Ask for Net 30 if you’re on Net 14. Ask for Net 60 if you’re on Net 30. Frame it as a partnership: “We’re planning to increase our order volume by 40% this year, and longer payment terms would help us commit to bigger orders.” Most suppliers would rather give you an extra 15 days than lose a growing account.

Run pre-orders for new collections. Instead of funding your entire next collection out of pocket, launch it as a pre-order. Collect payment upfront, use that cash to fund the production run, and deliver 4-6 weeks later. Brands like Australian fashion label Showpo built their early growth on this model. You get demand validation and cash flow in one move.

Switch to more frequent, smaller inventory orders. Instead of ordering 12 weeks of stock every quarter, order 4 weeks of stock every month. Yes, you might pay slightly more per unit, but the cash flow improvement is dramatic. You’re tying up a third of the capital at any given time. This works especially well with Australian or regional suppliers where lead times are shorter. For overseas suppliers, consider splitting your order into two shipments: 60% now, 40% in six weeks.

Clear slow-moving inventory aggressively. That stock sitting in your warehouse for 90+ days isn’t an asset, it’s a liability. Run a flash sale, bundle it with popular items, or move it through a marketplace channel at a lower margin. Getting 60 cents on the dollar back in cash today is almost always better than hoping to sell it at full price in three months. For a store with $100,000 in inventory, reducing dead stock from 15% to 8% frees up $7,000 immediately.

Reduce your BNPL exposure. Buy-now-pay-later services are great for conversion, but they delay your cash collection by 14-30 days and take a merchant fee of 4-6%. If BNPL represents more than 25-30% of your transactions, you’re carrying a significant cash drag. Consider limiting BNPL to orders above a minimum threshold, or running promotions that incentivise direct payment (a small discount for paying by card, for example). The math on this one often surprises people.

Set up a dedicated GST holding account. Open a separate bank account and transfer 10% of every sale into it automatically. When BAS time comes around, the money is sitting there waiting. This is such a simple tactic, but it eliminates one of the most common cash crunches Australian ecommerce businesses face.

Build a seasonal cash reserve. If your business has any seasonality at all (and most do), start building a cash reserve 6 months before your peak inventory purchase period. Set aside 5-10% of revenue each month into a separate high-interest savings account. When September rolls around and you need to place that big Christmas order, the cash is ready.

The Tool Stack That Makes This Automatic

You don’t need to manage all of this in a spreadsheet forever. Here’s the tool stack we recommend for Australian Shopify stores that want real-time cash flow visibility.

Xero as your accounting backbone. It’s the standard for Australian businesses, and it integrates natively with Shopify through apps like Link My Books or A2X. These connectors pull your Shopify transactions, fees, refunds, and payouts directly into Xero so your books are always accurate without manual data entry.

Float for cash flow forecasting. Float sits on top of Xero and automatically builds your cash flow forecast from your invoices, bills, and recurring expenses. It reads the expected payment dates on your bills and uses them to project when cash will move in and out. You can see exactly when you’ll dip below your target balance and model different scenarios (like “what happens if I place a $30K inventory order in week 6?”). Setting up Float takes about an hour once your Xero is clean, and from then on it updates automatically.

Inventory Planner or StockTrim for demand forecasting. These tools connect to your Shopify store and use your sales history to predict future demand per SKU. They’ll tell you exactly how much to order and when, factoring in lead times and safety stock. StockTrim is built in New Zealand and works particularly well for ANZ businesses. The payoff is immediate: smarter ordering means less cash locked in excess stock.

The integration chain works like this: Shopify sales data flows into Xero via Link My Books. Xero data flows into Float for cash forecasting. Inventory Planner pulls from Shopify to optimise ordering. Together, they give you a real-time picture of your cash position, your inventory health, and your upcoming commitments, without opening a single spreadsheet.

Cash Flow Red Flags: The Warning Signs Most Store Owners Miss

Most cash crunches do not arrive overnight. They build slowly over weeks, and by the time you notice, your options are limited. Train yourself to watch for these early warning signals in your weekly forecast, each one is a canary in the coal mine.

Your average days of inventory is climbing. If you had 35 days of inventory cover three months ago and now you are sitting at 55 days, stock is accumulating faster than it is selling. This is the earliest signal that a cash crunch is forming, because every extra day of inventory is cash locked up. Pull your Shopify inventory report monthly and chart this number. If it trends upward for two consecutive months, you need to either cut future orders or push harder on selling existing stock through bundles, flash sales, or marketplace channels.

Your ad spend is growing faster than your revenue. This happens gradually, you bump your Meta budget by $20/day here, add a TikTok campaign there, and before you know it, you are spending $2,000 more per month on ads but revenue has only grown by $1,500. The cash flow impact is worse than it looks because ad platforms bill immediately but the revenue trickles in over 3-7 days. Check your blended ROAS weekly. If it is dropping below 3x for more than two consecutive weeks, your ad spend is outpacing your returns and your cash position is eroding. For a framework on structuring your ad spend efficiently, see our guide on Meta Ads account structure.

Your credit card balance is climbing. Many store owners use credit cards to float the gap between ad spend and revenue collection. That works in the short term, but if your outstanding balance is growing month over month, you are spending future cash to fund today’s growth. Track your credit card balance on the same weekly dashboard as your bank balance. If it exceeds two weeks of revenue at any point, treat it as an emergency, the interest charges alone can eat 1-2% of your margin.

Your BAS liability is larger than your savings buffer. If your estimated quarterly GST liability exceeds what you have set aside in your holding account, you are using the ATO’s money to run your business. This is one of the most common reasons Australian ecommerce founders end up on payment plans, and the interest and late penalties add up quickly. Run the numbers at the end of each month, not just at BAS time. If the gap is growing, reduce discretionary spending immediately.

You are delaying supplier payments past their terms. If you are consistently paying suppliers at Day 35 on Net 30 terms, that is not clever cash management, it is a warning sign that your working capital is insufficient. Suppliers notice, and when they tighten your terms to prepayment or COD, your cash position gets worse, not better. The brands that negotiate the best terms are the ones who pay consistently within terms for 6-12 months before asking for an extension.

How It All Compounds Together

Here’s where this gets exciting. Each of these tactics works individually, but they compound when you stack them.

Say you’re doing $60K a month in revenue with a 60-day cash conversion cycle. You negotiate your supplier from Net 14 to Net 30 (saves 16 days). You switch from quarterly to monthly ordering (reduces average inventory holding by 15 days). You cap BNPL at 20% of transactions and push more customers to direct payment (saves 3-5 days on average DSO).

You’ve just compressed your cash cycle from 60 days to about 25 days. On $60K monthly revenue, that means you need roughly $50,000 in working capital instead of $120,000. That’s $70,000 freed up, cash you can put into ads, new product development, hiring, or simply keep as a buffer that lets you sleep at night.

And the 13-week forecast means you see all of this in advance. No more panic. No more “can we make payroll this week?” moments. No more missing out on inventory opportunities because you didn’t have the cash ready. You move from reactive to proactive, and that shift changes everything about how confidently you can grow.

The brands that scale to seven and eight figures aren’t just good at marketing or product, they’re good at understanding their unit economics and managing the rhythm of their cash. They know their numbers, they forecast religiously, and they treat cash management as a core business skill, not an afterthought.

If you want to go deeper on the cost side of the equation, check out our guide to reducing your cost of goods sold. And for the pricing decisions that directly impact your margins (and therefore your cash flow), our discount strategy guide breaks down how to run sales without destroying your profitability.

The Four Cash Flow Numbers to Check Every Monday Morning

Most founders check revenue daily and cash monthly. That is backwards. Revenue is a lagging vanity number, while cash is the thing that actually decides whether you can pay your supplier deposit in March. These four numbers take ten minutes to pull and will tell you more about the health of your store than a P and L ever will.

- Cash conversion cycle. Days inventory outstanding plus days sales outstanding minus days payables outstanding. A DTC store holding 90 days of stock and paying suppliers up front runs a cycle around 90 to 100 days, which means every dollar of growth eats roughly three months of cash. Getting that under 60 days is usually worth more than a 10% lift in conversion rate.

- Weeks of runway at current burn. Cash in the bank divided by average weekly net outflow. Under 8 weeks is a red flag. Under 4 weeks means you stop all discretionary spend today, including the ad test you were excited about.

- Inventory-to-cash ratio. The value of stock on hand against your bank balance. Once inventory exceeds roughly twice your cash position, you have quietly converted your business into a warehouse. Most Aussie stores that hit a cash crunch during a growth run got there this way, not through poor sales.

- Committed outflows for the next 30 days. Supplier POs, BAS, superannuation, payroll, rent and app subscriptions. List them with dates. The single most common cause of a surprise cash crunch is a quarterly BAS bill landing in the same week as a stock deposit.

Track these in one tab on a single spreadsheet and update it every Monday before you look at anything else. Ten minutes a week is cheaper than a bridging loan at 15% per annum.

The Cash Visibility Stack: Tools That Replace a Part-Time CFO

You do not need a finance hire at $2m in revenue. You need three or four tools that talk to each other and one recurring habit.

- Xero as the source of truth for accounts payable, receivable and BAS obligations. Set up tracking categories per sales channel so you can see which channel actually generates cash rather than just orders.

- A2X to reconcile Shopify payouts into Xero properly. Manual reconciliation of Shopify settlements is where most stores lose accuracy, because payouts net off refunds, fees and chargebacks into a single line.

- Float or Fathom for rolling 13-week forecasting on top of your Xero data. Both let you model a scenario, for example a 20% larger winter buy, and see the exact week your balance goes negative.

- Inventory Planner or Cogsy to link forecast demand to purchase orders, so your stock buys are driven by sell-through rate rather than a gut feel about the season ahead.

- Shopify Finance and your merchant statements to watch payment processing fees and chargeback ratios, both of which quietly compress margin as you scale.

The pattern that separates stores which scale calmly from stores which lurch between crises is not sophistication, it is cadence. A simple forecast reviewed weekly beats a beautiful model reviewed twice a year. If you want to see how cash discipline compounds into enterprise value, the Shopify exit readiness playbook covers how buyers actually price a store, and working capital efficiency sits near the top of that list. For the operational side of freeing up cash tied in stock, the Shopify 3PL playbook is a useful companion piece.

Your Next Step

Inside the eCommerce Circle, cash flow and financial clarity is one of the core pillars we work on with every member, because we’ve seen firsthand how many promising brands stall out not from lack of sales, but from lack of cash at the wrong moment. If you’re growing but feel like the financial side is running on gut feel rather than a system, we’d love to chat.