It is late May 2026, and somewhere in Australia a Shopify founder is about to discover that the inventory number on her balance sheet is wrong by $47,000. She does not know it yet. Her Cin7 dashboard says 312 of the navy wool crew. The warehouse has 264. The other 48 are scattered across a returns bay nobody zoned, a photo shoot box that never came back, a damaged carton in the corner, and two units that were probably never received. By the time she finds them on 28 June, her accountant has already filed.

What’s in This Article

This is what happens when a Shopify operator treats EOFY stocktake as a once-a-year tax chore instead of an operating reset. The count gets rushed. The variances get smoothed over. The dead stock gets carried into FY27 at full value, eating cash, eating margin, and eating the working capital that should have funded the spring reorder.

The Aussie founders who run stocktake properly do not see it as compliance. They see it as the one chance each year to reconcile reality with the system, to write down what the ATO will let them write down, and to walk into 1 July with a clean number and a real reorder plan. This playbook is the 5-phase system we run with hundreds of Aussie Shopify founders inside eCommerce Circle. There are 31 days until 30 June. Here is what to do with them.

Why Most Aussie Shopify Stocktakes Lose Money

Three numbers explain why this matters more than founders think.

The first is dead stock. A healthy retail business carries roughly 15% dead or slow-moving stock in active inventory. For DTC ecommerce brands, the figure typically creeps toward 33%. You bought it months ago, shipped it across an ocean, paid duty on it, and now it sits at full carrying cost waiting for a buyer who is not coming.

The second is carrying cost. Holding inventory costs roughly 20 to 30% of its value every year once you stack rent, insurance, capital cost, obsolescence risk, and the small fees that add up. Every $10,000 in dead stock is quietly costing you $2,500 a year in real money, before you even count the cash it is stopping you from spending on A-tier replenishment.

The third is shrinkage. The average retail shrinkage rate sits around 1.4%, with world-class operators below 0.2%. A $2 million inventory book at average shrinkage is leaking $28,000 a year. Half of that is preventable with cut-off discipline and a proper count. The other half tells you which SKUs to investigate before they bleed out further.

Add it up. A typical $1.5 million revenue Shopify brand carrying $400K in stock is sitting on around $130K in dead stock, $100K a year in carrying cost, and $5K to $8K in annual shrinkage. The EOFY stocktake is your moment to take a knife to that, claim what the ATO allows, and walk into FY27 with reality on your side. For more on the catalogue side of this work, see our companion piece on the Shopify SKU Rationalisation Playbook.

Phase 1: Pre-Count ABC Segmentation (Start 4 Weeks Out)

Counting every SKU with the same level of care is how teams burn three days and still finish with a sloppy result. The fix is ABC segmentation, run from your Shopify analytics 4 weeks before count day. The Pareto rule shows up almost perfectly in DTC inventory: roughly 20% of your SKUs drive 80% of revenue, and the other 70% of SKUs drive about 5%. They do not deserve the same count cadence, and they do not deserve the same level of risk treatment in your reconciliation.

Pull a trailing 90-day report from Shopify Admin under Analytics, then Reports, then “Sales by product”. Export to CSV. Sort by revenue contribution. Slice into three tiers:

- A-tier SKUs. Top 20% of products by revenue. These deserve a monthly cycle count year-round, and a 100% recount at EOFY. They are also your A-tier reorder priorities, so accuracy here is worth real money.

- B-tier SKUs. Next 30% by revenue. Quarterly cycle counts. Full count at EOFY but expect lower variance discipline.

- C-tier SKUs. Bottom 50% by SKU count, driving roughly 5% of revenue. Annual count only. Strong candidates for SKU rationalisation and dead stock write-down.

The segmentation also tells you something more useful. If your A-tier is only 12% of SKUs but they are driving 85% of revenue, you have an over-extended catalogue. If your A-tier is 35% of SKUs and you are still only at 70% of revenue, your hero is not a hero, it is part of a herd. Either way, the data sharpens your post-stocktake reset plan.

Phase 2: Cut-Off Discipline (72 Hours Before Count)

The single biggest source of bad stocktake variance is sloppy cut-off. Stock arriving on the dock but not yet receipted. Customer returns sitting in a bay but not yet booked back in. Cancelled orders that were picked but never put back. Pre-orders for FY27 that arrived early. Get cut-off wrong and your variance number is fiction.

Build a 72-hour cut-off discipline window before count day. The 3PL or warehouse runs in three modes during that window: receive, hold, count.

- T-72 hours: Receive everything in transit. Push the supplier to deliver any outstanding POs. Receive into Shopify (or your WMS) on arrival, not the next morning. Anything that misses the window goes into a clearly marked “FY27 stock” zone and does not get counted.

- T-48 hours: Clear the returns bay. Every customer return that has arrived must be inspected, graded, and either booked back into resaleable stock or written off as damaged. A returns bay full of unbooked stock is the number one reason variances cluster on top-sellers.

- T-24 hours: Freeze the picking floor. Pause new orders. Any picked-but-not-shipped orders sit in a quarantined zone with paperwork attached. They get counted as a single line, not lumped back into general inventory.

- T-0: Snapshot the system. Run “expected on hand” from Shopify or Cin7 Core at 8am count day. This is the number you reconcile against. Do not let any movement happen during the count itself.

This sounds heavy. It saves you days of variance investigation later. We have watched Aussie founders cut their EOFY reconciliation time from 11 days to 3 days by tightening cut-off alone. The free 30% retraining of your ops lead is the long-term bonus.

Phase 3: The Physical Count Itself

Count day starts before count day. Print the count sheets the afternoon before, with system quantities hidden. This is called blind counting and it is the only way to get a true count. If counters can see what the system says, they unconsciously calibrate toward it, and you lose the entire point of the exercise.

Use two-person teams on A-tier SKUs. One counts, one records. The recorder reads back the count before logging it. For B and C-tier, single counters are fine, but every line gets initialled. If you have a barcode scanner integrated with Cin7 Core or DEAR, run a scan-based count for A-tier and a sheet-based count for B and C. Mix the methods. Each catches different errors.

Zone the warehouse before count day. Aisle 1A, Aisle 1B, Aisle 2, and so on. Each team owns a zone. No team crosses into another zone until the lead has signed off the first. This stops the “wait, I think we already counted those” double-count problem that drove the variance on every Aussie founder’s first attempt.

The counted numbers go straight into the stocktake feature in your inventory system. Cin7 Core (formerly DEAR Systems) handles this well for Australian DTC operators because the stocktake mode automatically holds Shopify orders in a pending state while the count runs, so live sales cannot move the floor mid-count. Once you commit the stocktake, the adjustments push back to Shopify, the COGS journal posts to Xero or MYOB, and you have a clean audit trail for the accountant.

Phase 4: Variance Reconciliation and the ATO Write-Down Decision

Variance is the gap between what the system said and what you actually have. Every line of variance needs a reason code and a treatment. Without those, your accountant cannot defend the write-down if the ATO asks questions.

The ATO allows trading stock to be valued at the lower of cost, market selling value, or replacement value as at 30 June. Net realisable value (NRV) below cost is your friend on slow-moving and obsolete stock. If the resale price minus the cost to sell is below your cost price, you can carry it at the lower number and book the difference as a current-year deduction. This is one of the most under-used tax levers in Aussie ecommerce.

Use this four-bucket reconciliation framework on every variance line:

- Bucket 1: Adjust. Small variance, clear cause (mispick, miscount, receipt timing). Adjust to counted quantity. No write-down. No further action.

- Bucket 2: Write-down. Stock that exists but is worth less than book value. Slow movers, end-of-season carryovers, B-grade returns. Revalue to NRV. Photograph and document the reason. The difference is your deduction.

- Bucket 3: Write-off. Stock that no longer exists or has zero recoverable value. Damaged, expired, destroyed. Photograph, log the disposal method, retain the evidence for 5 years.

- Bucket 4: Investigate. Variance that does not match any known cause. Repeat shrinkage on a specific SKU or zone. Hold these lines out of the close, run a recount, then escalate to a security review if the pattern persists.

Small business operators get one more lever. If the total estimated change in trading stock value from opening to closing is less than $5,000, the ATO permits you to use opening stock as closing without a physical count. This is the “simplified trading stock rule” and it applies to entities with aggregated turnover under $10 million. Most growing Shopify brands blow past the $5,000 threshold quickly, but the rule is useful for very early-stage operators or for businesses with tiny on-hand stock.

Document everything. The ATO can and does challenge stock write-downs in an audit. Receipts, photographs, a written justification per line, and a board-approved policy on how you treat dead stock will save you in a review. The good news is that the documentation also becomes the management report you use to drive Q1 reorder decisions.

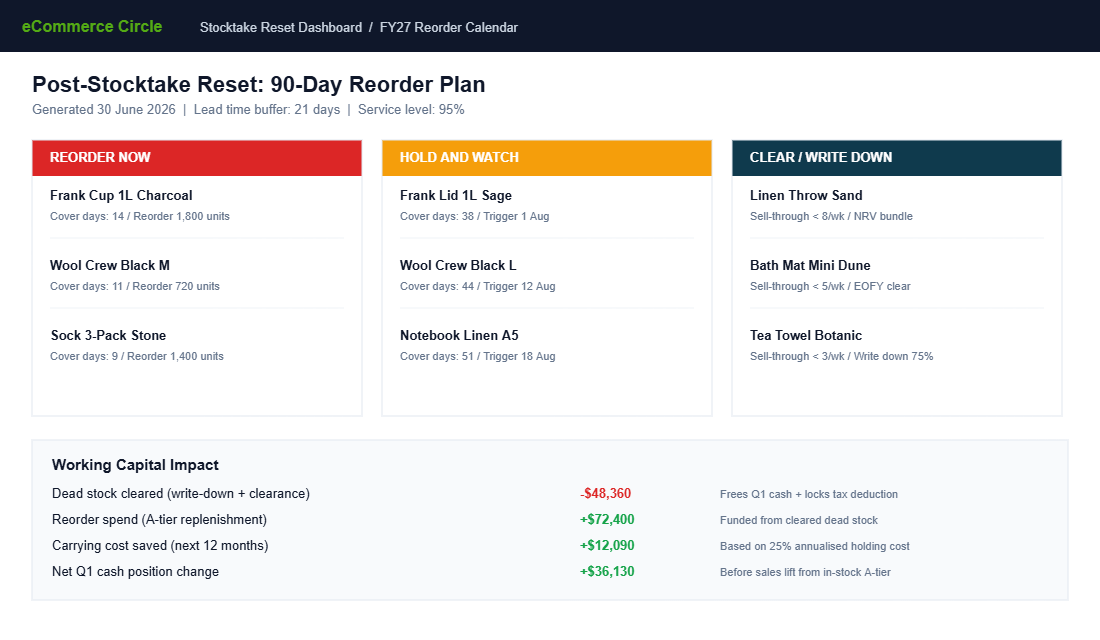

Phase 5: The Post-Stocktake Reset and FY27 Reorder Calendar

This is the phase 80% of Aussie founders skip, and it is the phase that pays the bills. A stocktake without a reset plan is just a tax compliance task. A stocktake with a reset plan is a working capital event.

The output of phase 4 is three lists: A-tier SKUs that need reorder now (cover days under 21), B-tier that need reorder triggers set (cover days 21 to 60), and dead stock that needs liquidation. The reset plan turns each list into action.

- A-tier reorder now. Place POs for any A-tier SKU with under 21 days of cover at current run rate plus the lead-time buffer. Use the cash freed up from dead stock clearance to fund these. This is non-negotiable.

- B-tier reorder triggers. Set reorder points in Cin7 Core or DEAR with safety stock equal to lead time times average daily sales times 1.25. Let the system trigger automatically. Founder does not need to be in the loop on B-tier replenishment past the trigger setup.

- Dead stock liquidation. Anything written down to 25% of cost or below needs a clearance path inside 60 days. Options: bundle into a quarterly clearance sale, ship to an outlet account, donate (which generates a deduction), or destroy with photo evidence. Pick a path per SKU and put a date on it.

Then build the FY27 reorder calendar. Mark the next four reorder windows for A-tier SKUs across the financial year, work backwards from peak season demand (BFCM, Christmas, Easter, Mother’s Day) to set PO drop dates, and lock the calendar into your team’s project tracker. The point of this calendar is to stop you ever scrambling for an A-tier reorder again. Pair it with our Cash Conversion Cycle Playbook to map the calendar to your cash position.

The Compound Effect: Why a Good Stocktake Becomes a CFO Move

Run this process once and you save the carrying cost on whatever dead stock you cleared. Run it three years in a row and something more interesting happens. You stop ordering the SKUs that always become dead stock. You start ordering more of the ones that always sell through. Your variance number drops because your team is calibrated. Your finance team trusts the inventory number on the balance sheet, which means your bank trusts the borrowing base, which means your line of credit expands.

The Aussie founders we coach who hit 95%+ inventory accuracy quarter on quarter end up with three structural advantages. They can take on bigger ad spend because their cash position is real, not theoretical. They can negotiate harder with suppliers because they know exactly what is moving. And they can run cleaner monthly business reviews because the COGS number ties out without three days of investigation. For the operating cadence around that, see our Monthly Business Review Playbook.

The brands you admire (Frank Green, The Oodie, Cultiver, Who Gives a Crap, Bared Footwear) treat inventory accuracy as a competitive edge, not a back office task. They count more often. They cycle count A-tier monthly. They run a proper EOFY ritual every year, not because the ATO requires it but because reality matters when you are scaling a brand.

The 31-Day EOFY Stocktake Checklist

Print this. Stick it on the wall. Walk through it with your ops lead this week.

- 4 weeks out (now, late May). Run ABC segmentation on the last 90 days. Confirm A-tier list. Brief the ops lead. Schedule count day (suggest Saturday 27 June, with a Tuesday 30 June recount window for variances).

- 3 weeks out. Audit master data. Every active SKU has a barcode, a cost price, a location, and a UOM. Anything missing gets fixed now, not on count day.

- 2 weeks out. Place the final pre-EOFY PO. Anything that will not land by 28 June goes into the FY27 zone and is excluded from the count.

- 10 days out. Inspect and clear the returns bay. Set up the quarantined zone for picked-not-shipped. Brief counters on blind-count protocol.

- 72 hours out. Cut-off discipline starts. Receive, hold, count modes activated.

- Count day. Two-person teams on A-tier. Single counters on B and C. Scanner backup on A-tier. No movement during the count.

- +3 days post-count. Variance reconciliation. Reason code every line. Photograph write-downs and write-offs. Commit the adjustment in Cin7 Core or your WMS.

- +7 days post-count. Reset dashboard built. Reorder now / hold / clear lists actioned. Liquidation paths set.

- +14 days post-count (mid July). FY27 reorder calendar locked. Cycle count cadence published. Monthly close runs clean.

If you can hit the last three items inside 14 days of count day, you are operating at the level of the top 10% of Aussie Shopify brands. Most founders stretch this to 8 weeks and lose the cash benefit by the time they finalise. The point of a tight EOFY stocktake is not the count itself. It is the speed from count to clean operating reset.

The other thing worth saying: the $5,000 small business stocktake exemption is genuinely useful for very small operators, and the permanent $20,000 instant asset write-off coming in from 1 July 2026 is worth a conversation with your accountant before 30 June. Neither replaces the discipline of an actual count if you are doing meaningful volume. Both can sit alongside the playbook above.

Inside eCommerce Circle, EOFY stocktake is one of the operating rituals we work on with every member during the May to July window. If you want a second opinion on yours, let’s talk.