You can do a million in revenue and still spend Tuesday morning on the phone with your bookkeeper, wondering why the bank account is light. The P&L looks fine. The Shopify dashboard says you had a record month. And yet the supplier deposit for the next container is due Friday and the maths is not adding up.

What’s in This Article

That gap, the one between profitable and liquid, is the single most punishing problem in Aussie DTC. The 2026 ASBFEO Pulse data shows one in six Australian SMEs now lose more than $2,500 a month to late payments, more than double what it was in 2024. One in four say cash flow is the thing that could kill them. Public DTC brands across 11 SEC filings sit at a median 133 days of inventory on hand. That is four and a half months of cash, frozen on a pallet in a Western Sydney 3PL, waiting to ship.

The brands that survive are not the ones with the best ads. They are the ones who treat working capital as a separate scoreboard from profit. They run a short cash conversion cycle (CCC), they negotiate supplier terms like a CFO, and they know exactly how many days their cash is locked up before it turns into another order. This playbook is the 5-lever framework we use inside eCommerce Circle to free up trapped cash without touching your P&L.

The Cash Conversion Cycle, In Plain English

The cash conversion cycle is the number of days between paying your supplier and getting that cash back from a customer order. It is the single most honest number in your business. Profit can be massaged. Revenue can be vanity. CCC is hard.

The formula is three pieces:

- Days Inventory Outstanding (DIO). Days you hold a unit before selling it. For Aussie DTC, this is the dominant driver.

- Days Sales Outstanding (DSO). Days between sale and cash in your account. For pure DTC, this is near zero because Shopify Payments settles in two to three business days. For B2B or wholesale, it can blow out to 45 plus.

- Days Payable Outstanding (DPO). Days between supplier invoice and you paying it. The median DTC brand sits at 36 days. The best operators get to 60 to 70 plus.

The maths is: CCC = DIO + DSO – DPO. A healthy DTC brand sits between 60 and 120 days. Anything below 60 is genuinely strong. Above 120 means too much working capital is sitting in inventory, and you will fund growth out of your own pocket every time you scale.

A worked example. A skincare brand doing $200K a month at 65% gross margin holds 90 days of inventory, gets paid by Shopify Payments in 3 days, and pays suppliers in 30 days. CCC is 90 + 3 – 30 = 63 days. Every dollar of sales takes 63 days to come back as cash available for the next inventory order. Cut DIO from 90 to 60 days and CCC drops to 33. On a $200K revenue base, that is roughly $130K of cash released back into the business, with zero impact on profit.

Lever 1: Cut Inventory Days With Ruthless SKU Discipline

Inventory is where most Aussie DTC brands trap their cash. The median public DTC brand is sitting on 133 days of stock. That is four and a half months of frozen capital. The fix is not “buy less”. It is buy smarter, more often, and only what the data tells you will sell in the next 60 days.

The 2026 vertical benchmarks give you a target. Fashion and apparel should be turning 4 to 7 times a year (52 to 91 days of stock). Beauty and cosmetics should be 4 to 9 turns (41 to 91 days). Supplements and consumables should turn 8 to 12 times (30 to 46 days). If your turnover ratio is below the bottom of this band, you have a working capital problem disguised as a stocking strategy.

Three moves that work in 30 days:

- Kill the bottom 20% of your SKU range. Pareto runs the world. Your top 20% of SKUs typically drive 70 to 80% of revenue. Mark the bottom 20% as “do not reorder”, run them to zero on a quiet promo, and reinvest that working capital in your hero products. Most brands have between 12 and 25 SKUs that should have been killed a year ago.

- Shorten your reorder cycle. If your supplier needs a 60-day lead time and a $20K minimum order, see if you can run a 30-day cycle with a $10K minimum at a 4 to 6% price premium. The premium feels expensive on a unit cost line. The cash flow win is enormous. You are turning the same dollar twice as often.

- Run a quarterly SKU rationalisation review. Bondi Sands, MCoBeauty, and Frank Body all run ruthless line edits. They launch a lot, but they kill faster than they launch. The brands that scale past $10M are not the ones with the deepest catalogue. They are the ones with the tightest one.

Tool stack: install Inventory Planner ($99 AUD per month for the starter tier, native to Shopify) or Stocky (free for Shopify Plus, $29 for everyone else). Both pull your sales history, calculate reorder points based on lead time and safety stock, and flag SKUs that are overstocked. The free version of Shopify’s native reports will tell you sell-through rate per SKU; that alone is enough to start the cull.

Lever 2: Negotiate Supplier Terms Like A CFO, Not A Buyer

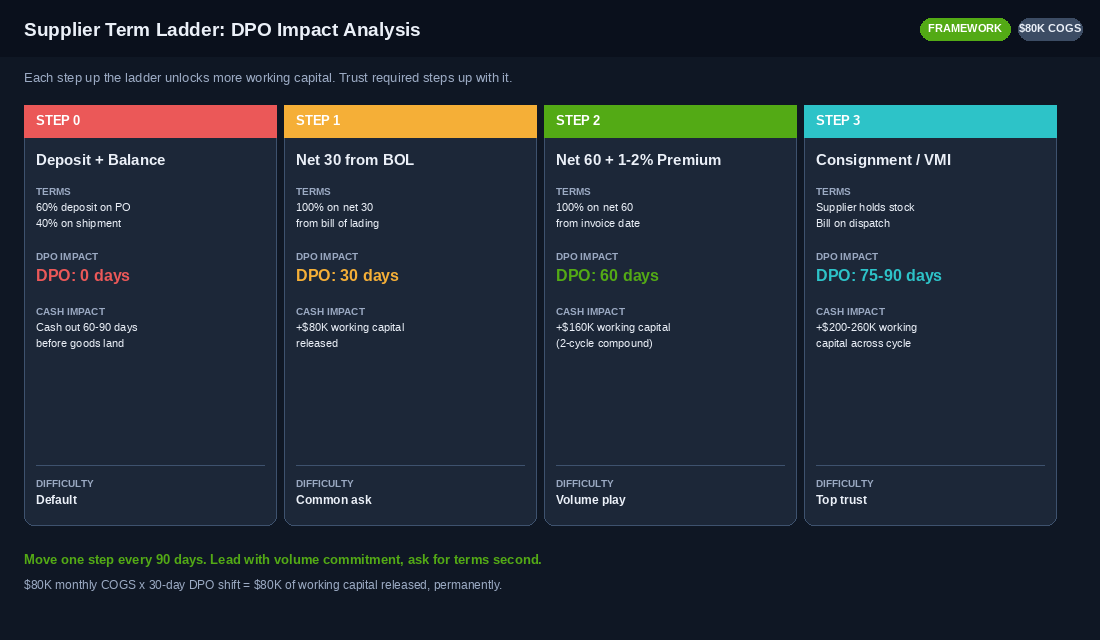

This is the single biggest lever most founders never pull. A 30-day shift in DPO (from net 0 to net 30, or net 30 to net 60) has the same effect on cash flow as a 30-day cut in inventory. The difference is, DPO costs you nothing. Your supplier is sitting on the same cash flow problem you are. They want the order locked in.

The framework we use inside Circle has four asks, in order of difficulty:

- Net 30 instead of deposit + balance. Most overseas suppliers default to 30% deposit, 70% on shipment. That puts your cash out 60 to 90 days before the stock lands. Ask for net 30 from bill of lading date. Many will say yes if you commit to a quarterly volume.

- Net 60 with a small price premium. If net 30 lands, run it for two cycles, then ask for net 60. Expect to pay a 1 to 2% premium. Worth it. You have just doubled your DPO.

- Consignment for slow movers. For inventory categories with longer turn rates (gift sets, seasonal lines), ask your supplier to hold the stock and bill on dispatch. They get the order. You get the cash protection.

- Hybrid local + offshore sourcing. Pair an Aussie or NZ supplier (faster lead time, smaller MOQ, 30-day terms) with your offshore manufacturer (lower unit cost, longer cycle). Use the local supplier to bridge stockouts. We covered the full negotiation playbook in the Shopify Supplier Negotiation Playbook.

The cash impact: on a brand spending $80K a month on COGS, every 30-day shift in DPO frees up roughly $80K of working capital permanently. That is not a one-off win. It is $80K that lives in your bank account every single month from then on.

Lever 3: Tighten The DSO Side (Payments, Wholesale, Marketplaces)

For most pure DTC Shopify brands, DSO is a non-issue. Shopify Payments settles in two to three business days. PayPal in one. Klarna and Afterpay pay you upfront and carry the customer credit risk themselves.

But the moment you add wholesale, B2B, or marketplace channels, DSO becomes a serious working capital drag.

- Wholesale. Standard retail trade terms in Australia are net 30 to net 60 from invoice date. With shipping and processing time, real DSO often lands at 50 to 75 days. If 30% of your revenue is wholesale at 60-day terms, your blended DSO is 18 days higher than a pure DTC peer.

- Amazon AU. Settlement runs on a biweekly cycle, but the reserve policy holds 3 to 5% back for 14 days. Effective DSO sits around 14 to 21 days.

- Marketplaces and dropship partners. Catch, Iconic, MyDeal, and Kogan vary widely. Some pay weekly, some net 60. Read the contract before you list. We have seen brands lock up $40K to $80K on a marketplace push that, on paper, looked like a great channel.

Three moves that compress DSO:

- Early-payment discounts for wholesale. Offer 2% off net 7 instead of net 30. Half your accounts will take it. The 2% cost is far cheaper than the working capital squeeze.

- Use the Shopify B2B app for prepayment. Shopify’s native B2B feature lets you set per-customer payment terms, including “payment due on order”. Force prepayment for new accounts, and only extend terms after 90 days of clean trading.

- Invoice finance for the rest. Octet, Earlypay, and Scottish Pacific are the main Aussie invoice finance providers. They will advance 85 to 90% of an invoice within 24 hours. Cost is 1 to 3% of the invoice value depending on the term. For a $200K wholesale order at net 60, you are looking at $4K to $6K to get the cash 60 days earlier.

Lever 4: Pre-Order, Waitlist, And Drop Models (Cash Before COGS)

The dirty secret of working capital is that the best brands have already broken the equation. They collect cash before they pay for goods. This is not new (Apple, Tesla, and Supreme have all run negative CCC models for years). It is now well within reach for Aussie DTC.

The four pre-order plays that work on Shopify in 2026:

- Hero product pre-launch. Build a waitlist for 4 to 6 weeks. Run paid traffic to a landing page with email capture. When you go live, the first 48 hours of orders fund the production run. We have seen Aussie DTC brands collect $40K to $120K in pre-orders, then pay the supplier deposit out of that float.

- Drop model for new colourways or limited runs. Set a drop date, sell on that date only, ship in 4 to 6 weeks. The pre-order cash funds the entire production cycle. Best for fashion, accessories, and lifestyle categories.

- Subscription with a paid trial. Charge for the first month upfront, ship monthly. Cash is in your account 28 days before you incur fulfilment cost for the next box. Aussie subscription operators routinely run negative working capital this way.

- Bundle pre-sale at a discount. Offer a 10 to 15% saving for a customer who pre-orders a bundle, with a ship date 4 weeks out. The cash discount is far cheaper than financing the same working capital through a Wayflyer advance.

Set up: native Shopify pre-orders work with the PreOrder Globo ($14.95 AUD per month) or PreProduct ($24.99 per month) apps. Both let you set a partial deposit (we recommend 30 to 50%), set the ship date on the product page, and trigger an automated email cadence that warms the customer through the wait. Klaviyo handles the waitlist email flow natively if you connect via the Shopify Klaviyo Inventory feed.

Lever 5: Use Working Capital Financing Like A Tool, Not A Crutch

If you have done the first four levers and still have a structural cash gap, financing is a legitimate tool. The mistake most founders make is using debt to paper over an operational problem (slow turns, sloppy supplier terms, a bloated SKU range). Financing only works if your unit economics are strong and your CCC is moving in the right direction.

The 2026 Aussie ecommerce financing stack:

- Shopify Capital. Available to Aussie merchants from $200 to $2M AUD. Underwritten on your Shopify sales history, no personal guarantee, no credit check. Repayment is a flat percentage of daily sales (typically 12 to 17%). Effective annualised rate sits at 18 to 28%. Fast, zero-friction, but the cost compounds if you take it before your CCC is healthy.

- Wayflyer. Operates in Australia. Funding limits from USD $5K to $20M, sized at 1.5 to 3 times average monthly revenue. Term loan or rolling 12-month facility. Better rates than Shopify Capital at higher volume, plus they bundle in analytics on your Meta and Klaviyo data.

- Invoice finance (Octet, Earlypay). For brands with material wholesale or B2B revenue. Advances 85 to 90% of an invoice within 24 hours.

- Trade finance from your bank. CBA, NAB, ANZ, and Westpac all offer ecommerce-specific trade facilities once you are doing $1M+ annual revenue. Letters of credit, FX hedges, and import finance. Rates are sharper than non-bank lenders, but the application is slower.

The discipline test: never use external financing to fund inventory that has not validated demand. Only deploy financing capital against your top-selling SKUs with proven sell-through and a tight reorder cycle. If you use debt to fund a SKU expansion or a new category test, you are betting cash against an unvalidated hypothesis. That is the path to a $300K debt balance and a warehouse of dead stock.

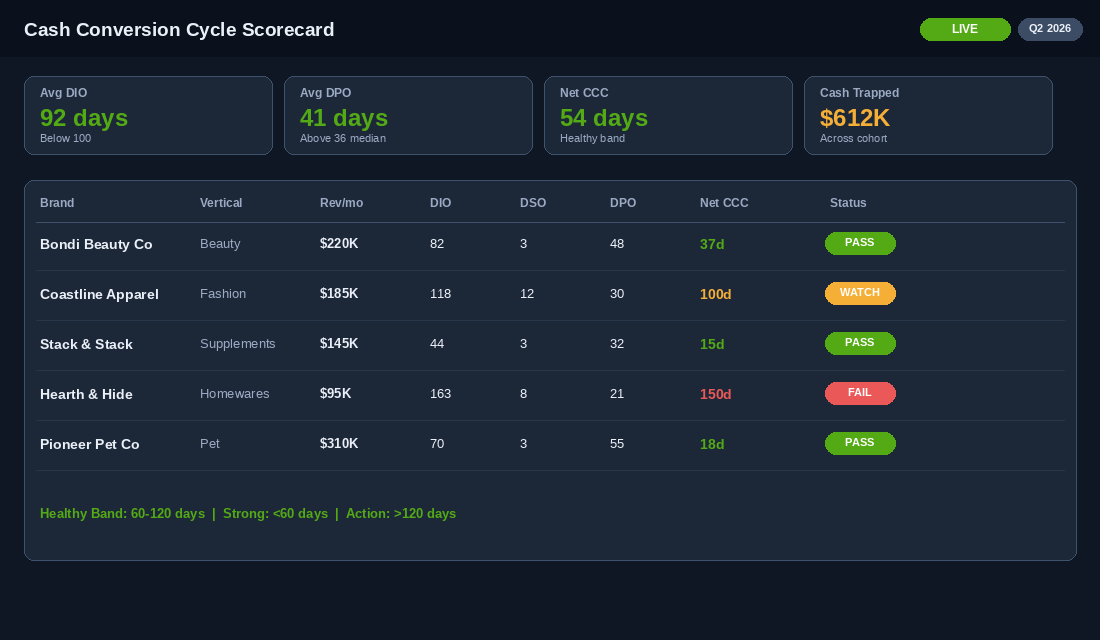

The Compound Effect: A .4M Brand Walks Through The Maths

Let me ground this in a real case. We worked with a Melbourne-based beauty brand doing $1.4M annual revenue, 62% gross margin, 45% net of marketing. Profitable on paper. Cash account was sitting at $38K against a $180K monthly burn. They were one bad month away from a problem.

The CCC audit showed:

- DIO: 118 days (well above the beauty benchmark of 41 to 91)

- DSO: 3 days (clean, all DTC via Shopify Payments)

- DPO: 21 days (well below the 36-day median)

- Net CCC: 100 days

Over 90 days, we ran the 5 levers:

- Lever 1. Killed 14 of 47 SKUs. Reinvested the working capital into the top 12 SKUs. DIO dropped from 118 to 82 days.

- Lever 2. Renegotiated terms with two of three suppliers. DPO moved from 21 to 48 days.

- Lever 3. Not needed (100% DTC).

- Lever 4. Launched a pre-order on the new hero range. Collected $62K in pre-orders, funded 70% of the production run before the supplier deposit.

- Lever 5. Took a $80K Shopify Capital advance to cover the gap on Q4 stock-up. Repaid in 5 months. Net cost: $11K.

The result: CCC fell from 100 days to 37 days. Working capital released back into the business: $182K. The bank account ended the next quarter at $221K, not $38K. The brand went from one bad month away from a problem to genuinely capitalised. Same revenue. Same profit. Different liquidity.

The 90-Day Working Capital Rollout

Here is the sequence we run inside Circle. Do not try to do all five levers at once. The point is compounding wins, not heroics.

- Week 1. Calculate your current CCC. Pull cost of goods, average inventory, average payables, and DSO from your Xero or QuickBooks. Build the single-page CCC dashboard. Most founders have never done this.

- Weeks 2 to 4. Run the SKU cull (Lever 1). Identify the bottom 20%, set a discounted clearance, and pull them from reorder. Update Inventory Planner or Stocky with the new mix.

- Weeks 3 to 6. Start the supplier conversation (Lever 2). Lead with the volume commitment, not the term ask. “We want to commit to Q3 and Q4 orders at this volume. Here is the schedule. To make that work, we need net 30 from BOL date.”

- Weeks 4 to 8. If wholesale or B2B is part of your mix, run the DSO audit (Lever 3). Tighten terms for new accounts, introduce early-payment discounts, and price in invoice finance for the long-paying customers.

- Weeks 6 to 10. Plan and launch a pre-order or waitlist drop (Lever 4). Use it to fund your next big production run.

- Weeks 8 to 12. Only after the operational levers are working, evaluate financing (Lever 5). Match the financing instrument to the use case.

Track CCC weekly. Put the number on the wall. Do not let it drift back. The whole point of this work is that the gains are permanent. You do not need to repeat the exercise. You just need to defend it.

Three Failure Modes To Avoid

The brands that try this and fail tend to do one of three things:

- Cut inventory too aggressively, then stock out. Stockouts on hero SKUs cost more in lost contribution than slow turns cost in working capital. The fix: cut SKU breadth, not depth. Keep your top sellers deep. Cut the tail.

- Use Shopify Capital to fund growth without fixing CCC first. Debt does not solve a slow inventory turn. It compounds it. Run the operational levers first, then layer financing on top.

- Treat the CCC dashboard as a one-time audit. CCC creeps. Suppliers tighten terms when their own cash flow gets squeezed. A new product launch can blow out inventory days for a quarter. Review CCC monthly inside your Monthly Business Review.

Why This Compounds With Everything Else

The cash conversion cycle is the meta-metric that sits above CR, AOV, ROAS, and contribution margin. You can have a 4% conversion rate, $120 AOV, and a 32% contribution margin, and still be technically insolvent because all your cash is in a container.

Tighten the CCC, and every other lever in the business gets stronger. You can take on inventory bets faster. You can fund a Meta ads push without dipping into credit. You can negotiate harder with suppliers because you are not desperate. You can buy back equity from an early investor. You can pay yourself. The same brand, with the same revenue and the same profit, becomes a fundamentally different business once it is liquid.

The brands that scale past $5M, $10M, $20M in revenue without diluting equity all run a tight CCC. The brands that stall out, or worse, fold while showing P&L profits, almost always do so because they ran out of cash, not customers. The 5-lever framework is how you stay on the right side of that line.

Inside eCommerce Circle, working capital and cash conversion is one of the core pillars we work on with every member, alongside the broader CAC Payback Period Playbook and the unit economics work that sits underneath it. If you want a second opinion on your CCC, let’s talk.