A refund is the politest way a customer ever fires you. The money goes back, the parcel comes back, and most founders file the whole thing under business as usual.

What’s in This Article

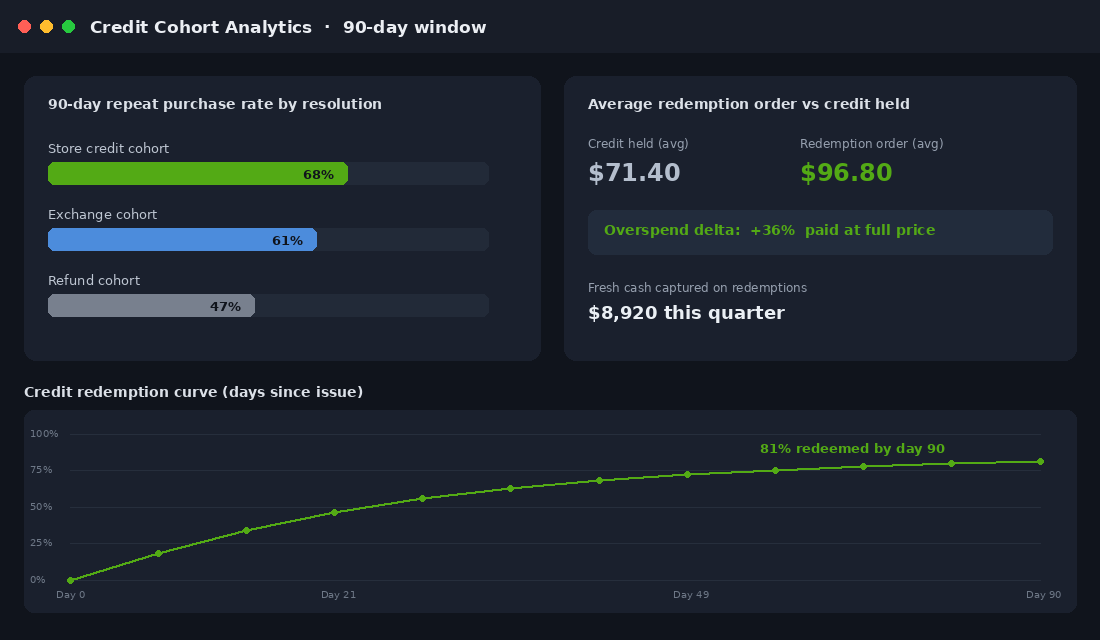

Here is the number that should change how you see it: roughly 68% of customers who receive store credit come back and buy again. After a cash refund, that figure drops to somewhere between 45 and 50%. Same product, same customer, same complaint. The only thing that changed is what you handed them on the way out the door.

Most Aussie Shopify stores hand over cash by default, because that is what the refund button does. The brands that are serious about retention treat every return as a fork in the road. One path sends the revenue and the customer out the door together. The other keeps the money inside the business as a credit the customer is now motivated to come back and spend.

This playbook covers the 5-move system for doing that properly on Shopify: getting the legal line right under Australian Consumer Law, making credit the most attractive exit in your returns flow, running the economics, building it with Shopify’s native store credit, and then using credit as a retention currency well beyond returns.

Why a Refund Is the Worst of Your Three Outcomes

Every return request has three possible endings, and they are not created equal.

- An exchange keeps the revenue and keeps the product in the customer’s hands. Best outcome, but only works when the fix is a different size or colour.

- Store credit keeps the revenue in your business and creates a reason for a second visit. The customer now has money that only works in one shop: yours.

- A cash refund sends the revenue back, eats your original shipping and payment fees, and leaves the customer free to spend the money with the competitor who retargets them tomorrow.

The encouraging part: customers are far more open to the middle option than most founders assume. Around 60% of shoppers say they would accept an exchange or store credit instead of a refund, provided the process is fast and convenient. They do not need to be tricked into it. They need it to be the easy, obvious, slightly more generous path.

If your returns volume itself is the problem, start with the returns reduction playbook first. This article is about what happens to the returns you cannot prevent.

Move 1: Get the Legal Line Right (Before You Touch Your Policy)

Store credit sits right on top of a line that the ACCC polices hard, so get this clear before you change anything.

Under Australian Consumer Law, when a product has a major failure, the customer chooses the remedy. Refund, repair, or replacement, their call. You cannot force store credit on a faulty product, and a policy or sign that says otherwise is unlawful. That includes the classic “no refunds” sign, which the ACCC treats as misleading because it implies refunds are never available.

Change of mind is a different universe. The ACL does not require you to accept change-of-mind returns at all. Wrong size guesses, “it looked different online”, impulse regret: none of that triggers a legal right to a refund. Which means everything you offer for change of mind, including store credit, is voluntary policy. You set the terms, and credit can absolutely be the headline remedy.

One nuance worth knowing: gift cards you sell in Australia must be valid for at least three years. Store credit issued for a returned item is generally treated as a credit note rather than a sold gift card, so the three-year rule does not automatically apply. Showpo, for example, runs 12-month expiry on its return credit. Whatever expiry you pick, state it clearly at the moment you issue the credit, and apply it consistently.

The practical rule: build two lanes in your returns flow. A faulty-item lane where the customer picks the remedy and a refund is offered without friction, and a change-of-mind lane where store credit is the default and the most rewarding option. We covered the broader compliance picture in the Shopify consumer law playbook; this article assumes the faulty lane is already honest.

Move 2: Make Credit the Most Attractive Exit in Your Returns Flow

Nobody chooses store credit out of loyalty to your P&L. They choose it because the offer in front of them is faster, easier, or worth more than the refund. You have three levers to make that true.

Lever 1: Speed. A card refund takes 3 to 10 business days to land, and the customer knows it. Store credit can be instant. Issue it the moment the return is approved or the parcel is scanned at lodgement, not when it lands back at your 3PL. “Spend it right now” beats “wait a week for your bank” for a meaningful slice of shoppers.

Lever 2: Bonus value. This is the lever with the published numbers behind it. When brands attach a bonus to credit, acceptance rates typically land between 40 and 60% of eligible returns. Showpo made this famous in Australia with its 110% store credit offer: return for credit and get 10% extra on top, while cash refunds are only available in the first 7 days. The 10% bonus costs far less than it looks, because you only pay it in margin terms if the credit is redeemed, and redeemed credit drags a full-price order along with it.

Lever 3: Fee asymmetry. Princess Polly charges $6.95 for a refund return label, while returns for a gift card or exchange ship free. The message lands without a single line of persuasion copy: cash costs you, credit is free. You do not need to copy the exact numbers, but the structure (refund carries the friction, credit carries none) is the proven pattern.

Present the options in this order on your returns portal: exchange first, store credit second with the bonus badge, refund last. Never hide the refund option where the customer is legally entitled to one. You are stacking the deck, not rigging the game.

Move 3: Run the Credit Economics Before You Set the Bonus

Store credit only works if the maths works, so run your own numbers before you pick a bonus percentage. Here is the worked example for a typical apparel store.

Take an $80 change-of-mind return. The refund path returns $80 to the customer, and you also wear the original payment processing fee and shipping. Revenue kept: zero. Now run the credit path with a 110% offer: you issue $88 in credit. Customers who redeem credit reliably overspend it. The benchmark: a customer holding $50 of credit typically spends $65 to $75 on their next order, a 30 to 50% top-up paid at full price. On the $88 credit, that looks like a $110 to $120 order, with the gap above the credit hitting your bank account as fresh cash.

Three economics rules keep this honest:

- Treat issued credit as a liability, not revenue. It is money you owe in product. Track the outstanding balance monthly the same way you track gift card liability, a discipline we covered in the gift card revenue playbook.

- Price the bonus against your margin, not your gut. At a 60% gross margin, a 10% credit bonus costs you 4 cents of margin per dollar of credit redeemed. At a 30% margin, the same bonus costs 7 cents and the overspend has to carry more weight. Thin-margin stores should start at 5% bonus, not 15%.

- Expect partial redemption. Healthy programs see 70 to 85% of credit redeemed within 90 days. The remainder is breakage. Do not budget on it, but do not pretend it is zero either.

Move 4: Build It With Shopify’s Native Store Credit (15 Minutes, No App Fees)

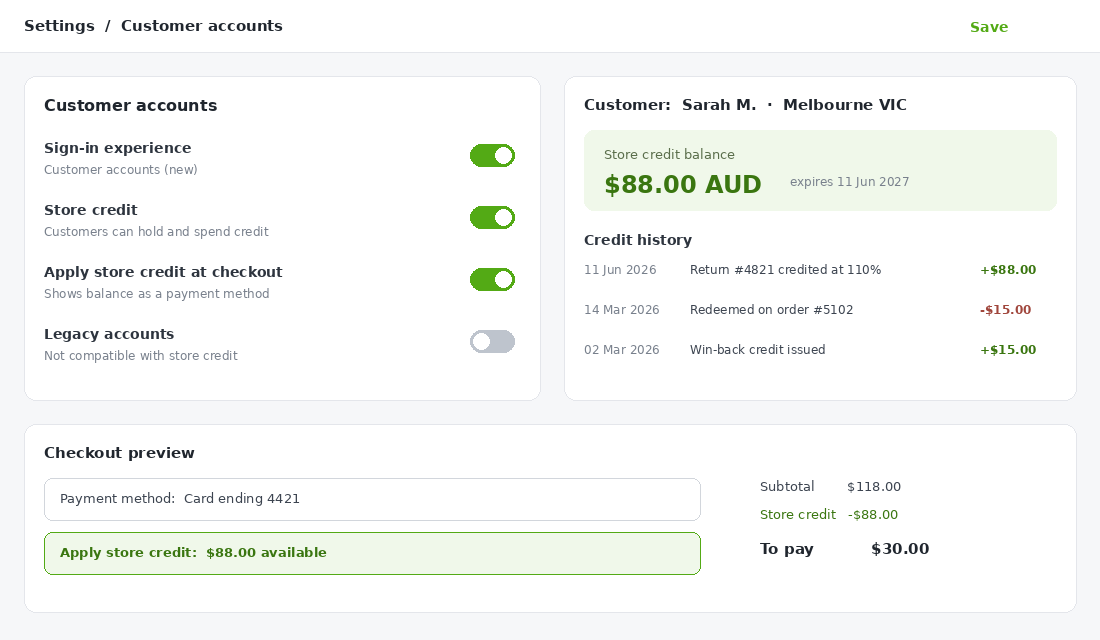

Until 2024 you needed an app for any of this. Shopify now has store credit built into the platform, and for most stores under about $150k a month it is all you need to start. Credit lives on the customer’s account as a real payment method they can apply at checkout.

Setup takes five steps:

- In Shopify admin, go to Settings, then Customer accounts, and make sure you are on the new customer accounts experience. Native store credit does not work on legacy accounts, and this is the step that catches most older stores.

- In the same screen, switch on the Store credit toggle.

- In Settings, then Checkout, confirm Apply store credit is active so signed-in customers see their balance as a payment option.

- To issue credit manually, open any customer profile and add a store credit amount directly. For returns volume, wire your returns portal or flow so approved change-of-mind returns issue credit automatically.

- Place a credit balance reminder in your account page and post-issue email so the customer never has to wonder where the money went.

One gotcha worth flagging: for Shopify stores created on or after 12 May 2025, third-party transaction fees apply to the portion of an order paid with store credit, unless you are on Shopify Plus with Shopify Payments active. It is not a deal-breaker, but it belongs in your margin maths from Move 3.

When to graduate to an app: native credit issues and redeems, but it does not run programs. If you want automatic bonus percentages, cashback rules, credit expiry, or bulk campaigns, that is where a dedicated tool like Rise.ai earns its keep. Rise’s own case studies claim results like a 33% lift in repeat customer rate for US activewear brand Wodbottom after switching coupon rewards to store credit, and a 9% AOV lift from a “spend $75, get $10 credit” promotion. Treat those as vendor numbers rather than gospel, but the direction matches what the independent data says about credit versus discounts.

Move 5: Turn Credit Into a Retention Currency Beyond Returns

Once the rails exist, returns are just the first use case. Store credit outperforms an equivalent discount code in almost every retention play, for one psychological reason: a discount is marketing, but credit is money the customer already owns. People delete 15%-off emails all day. They do not forget about $20 sitting in their account.

Four places to deploy it:

- Win-back campaigns. Swap the tired “15% off your next order” in your lapsed-customer flow for “$15 credit is waiting in your account, it expires in 30 days”. Ownership plus a deadline beats a generic discount. Wire it into the sequence from our win-back flow playbook.

- Cashback instead of points. A simple “earn 5% back in credit on every order” program is easier to understand than a points scheme and keeps the reward spendable only with you.

- VIP surprise drops. An unannounced $20 credit to your top decile of customers costs less than most VIP gifting and lands as a gesture, not a promo.

- Service recovery. Late parcel, damaged box, support hiccup: a small instant credit converts a complaint into a reason to come back, without touching cash.

Whatever you deploy, build the expiry reminder sequence in Klaviyo: a reminder at 30 days out, 7 days out, and 24 hours before expiry. Unredeemed credit earns you nothing. The reminder emails routinely outperform campaign sends because the subject line is about the customer’s own money.

Where Store Credit Does Not Fit

Credit is not a universal answer, and pushing it where it does not belong burns trust. Three situations where you should reach for something else:

- One-and-done products. If your customer genuinely buys once every few years (think luggage or a single-purchase device), credit has nowhere to go. An exchange or a clean refund serves you better than a credit that expires unredeemed and leaves a sour taste.

- High-ticket considered purchases. Asking someone to hold $600 in credit against a future order they may never plan is a big ask. Above roughly $300, offer split remedies: part refund, part bonus credit, and let the customer choose the mix.

- Customers showing return-abuse patterns. Serial returners will happily farm a 110% bonus. Cap bonus credit at one or two uses per customer per quarter, and route flagged accounts to standard refunds. Your returns data already knows who they are.

For everyone else, which in apparel, beauty, and consumables is the overwhelming majority of your returns queue, credit-first is simply the better default for both sides: the customer gets more value faster, and you keep the relationship alive.

The Compound Effect: What This Is Worth on a Two Million Dollar Store

Run the system end to end on a $2M-a-year apparel brand doing roughly 1,750 orders a month at a $95 AOV. At a 20% return rate, about 350 orders come back each month, call it $33,000 of revenue at the door.

Today, if everything is refunded, that $33,000 leaves every month. Now run the playbook: half of eligible returners take the credit offer (inside the published 40 to 60% take-rate band), so roughly $16,500 stays in the business as credit each month. Around 80% of it gets redeemed within 90 days, and redeemers top up their orders by about 30% at full price, adding roughly $4,000 of fresh revenue on top.

That is in the order of $200,000 of annual revenue that used to walk out the door, now staying inside the business, before you count the second-order effect: the credit cohort comes back at roughly 68% instead of the refund cohort’s 45 to 50%, and every one of those recovered customers has a lifetime value attached, not just one rescued order.

The Accounting Side: GST, Breakage, and What Your Books Need to Show

Store credit is not revenue when you issue it. It is a liability sitting on your balance sheet until the customer spends it, and getting this wrong creates two problems: a P&L that flatters your refund months, and a GST position your accountant has to unwind at BAS time.

- Issuing credit reverses the sale. When you refund to credit, the original sale’s GST is adjusted and the credit sits as unearned revenue. The GST obligation fires again when the credit is redeemed. Xero and MYOB both handle this cleanly if your Shopify integration maps gift card and store credit transactions to a liability account, not a sales account. Check that mapping this week, because the default on some connectors is wrong.

- Track your redemption rate and breakage honestly. Across Aussie DTC programs, 75 to 90% of store credit gets redeemed within 12 months. The unredeemed remainder (breakage) eventually gets recognised as revenue, but only once redemption is remote, and your 3-year expiry term under Australian Consumer Law sets the earliest realistic horizon for most of it.

- Watch the liability balance monthly. A growing credit balance is deferred demand, which is good, until it is deferred into a quarter where you have already spent the cash. If outstanding credit exceeds 1.5 to 2% of trailing 12-month revenue, factor it into your cash forecast the same way you would a wholesale order book.

None of this is a reason to avoid store credit. It is a reason to set up the bookkeeping before the program scales, because retrofitting six months of mis-mapped credit transactions at EOFY is an expensive conversation with your accountant. Speaking of which: this section is general guidance, not tax advice. Run your setup past your accountant before BAS time.

The Four Mistakes That Sink Store Credit Programs

- Forcing credit on faulty goods. The fastest way to an ACCC complaint and a public spray on ProductReview. Faulty lane: customer picks. Change-of-mind lane: credit leads. Never blur them.

- Burying the balance. If the customer has to email support to find out what credit they hold, redemption craters. Balance on the account page, in the issue email, and in reminders.

- A bonus too small to change behaviour. A 2% sweetener moves nobody. The published take rates come from offers in the 10% range. If your margin cannot fund 10%, fund speed and free return shipping on the credit option instead.

- Counting issued credit as won revenue. It is a liability until redeemed. Celebrate redemption and overspend, not issuance.

The Five Numbers to Check Every Monday

- Credit take rate on eligible change-of-mind returns. Target 40 to 60% with a real bonus attached.

- Redemption rate within 90 days. Healthy is 70 to 85%. Below that, fix your reminders and balance visibility.

- Overspend delta: average order value of credit redemptions versus credit issued. Target 25 to 40% above the credit amount.

- Cohort repeat rate: 90-day repeat purchase rate of credit takers versus refund takers. This is the number that proves the program.

- Outstanding credit liability: total unredeemed balance. Watch the trend, not the absolute number.

Your 30-Day Store Credit Rollout

- Week 1: Audit your returns policy against the two-lane rule. Fix any wording that could read as denying refund rights on faulty goods. Decide your credit expiry and write it into the policy.

- Week 2: Switch on Shopify native store credit (five steps above). Test the full loop yourself: issue credit, sign in, redeem at checkout.

- Week 3: Restructure the returns portal: exchange first, credit with bonus second, refund third. Set your bonus using the Move 3 margin maths. Add the fee asymmetry if it suits your brand.

- Week 4: Build the Klaviyo pieces: credit-issued email with balance, expiry reminder sequence, and swap your win-back discount for a credit offer. Set up the five Monday numbers in a simple sheet.

Run it for a full quarter before judging it. Returns are seasonal, and the cohort repeat effect needs 90 days to show up in the numbers.

Inside eCommerce Circle, retention economics like this is one of the core pillars we work on with every member. If you want a second opinion on your returns flow and where credit fits, let’s talk.