You shipped the order. The customer got the product. Six weeks later your payment processor pulls the money back out of your account, adds a fee on top, and there is nothing in your inbox explaining why. That is a chargeback, and if you run a Shopify store in Australia long enough, it will happen to you.

What’s in This Article

Most founders treat chargebacks as a cost of doing business. They glance at the dispute email, decide it is not worth the fight, and click accept. That instinct is quietly draining your margin. Card fraud on Australian-issued cards hit $913 million in 2024, up 20% on the year, and card-not-present fraud (the kind that lands on online stores) made up 90% of all card payments fraud. This is not a rounding error any more. It is a tax on every store that has no system to fight back.

Here is the part that should change how you think about it. Every dollar lost to a chargeback actually costs you between $3.75 and $4.61 once you add the lost product, the original processing fees, the dispute fee, and the staff time. The brands that protect their profit do not have less fraud than you. They have a defence system. This is that system, built into four layers you can set up on a Shopify store this week.

Why Chargebacks Are the Silent Margin Killer

A chargeback is not a refund. When you refund a customer, you control it, you keep the relationship, and you pay back exactly what they spent. A chargeback is the customer’s bank reversing the payment over your head, and the card networks charge you a fee (usually $15 to $25 AUD) whether you win the dispute or not.

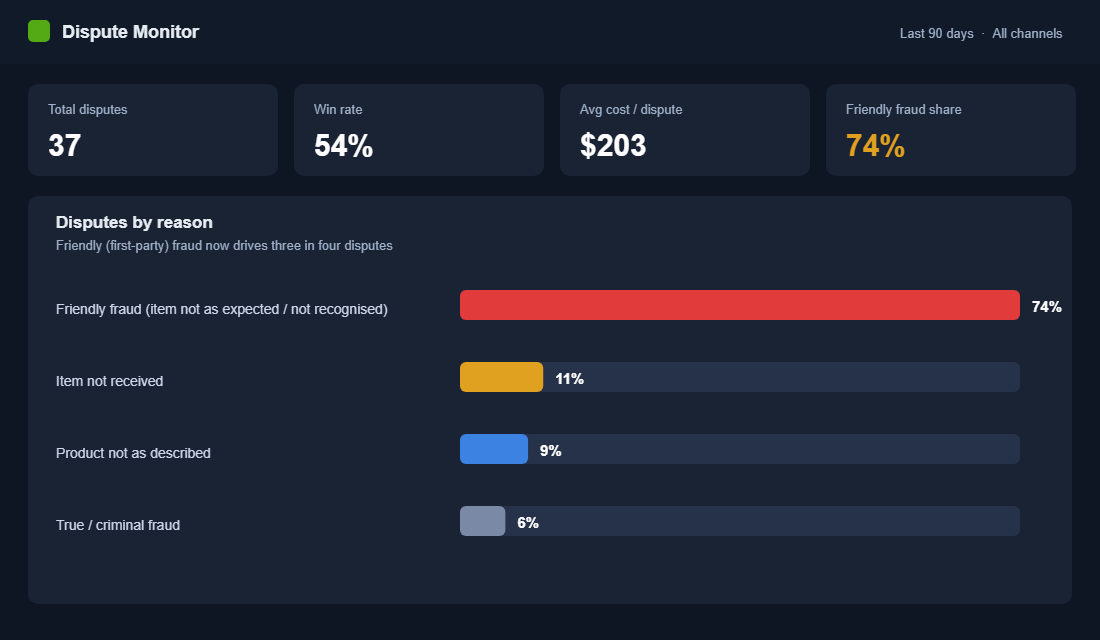

The volume is climbing fast. One analysis found a 233% increase in retail ecommerce chargebacks between Q1 and Q3 of 2025, fuelled by “refund hack” tutorials doing the rounds on TikTok. Roughly 1 in 5 consumers now say they would justify filing a false claim. Globally, chargebacks are forecast to grow from $33.79 billion in 2025 to $41.69 billion by 2028.

Run the numbers on a single dispute and the picture sharpens. Say you sell a $180 order at a 30% margin, so $54 of profit. A chargeback claws back the full $180, adds a $20 dispute fee, and you have already paid the supplier and the freight. At the all-in cost multiple, that one reversed order does not wipe out $54 of profit. It wipes out the profit on three or four clean orders behind it. That is why a 1% chargeback rate hurts far more than it looks on a spreadsheet.

The most dangerous part is who is actually filing them. The classic picture of a chargeback is a stolen card. The reality in 2025 is “friendly fraud”, where a real customer disputes a real purchase they made. First-party (friendly) fraud now drives around 75% of ecommerce disputes. That changes everything about how you defend, because you cannot block your own paying customers at the door. You have to manage them through the whole journey instead.

The 4-Layer Defence System

Stopping chargebacks is not one tactic. It is four layers, each catching what the layer before it missed. Skip a layer and the leaks find their way through. Here is the full stack before we break each one down:

- Layer 1: Screen the order. Stop the obviously fraudulent transaction before you ship it.

- Layer 2: Remove the excuse. Kill the confusion and friction that turns honest customers into friendly fraudsters.

- Layer 3: Win the dispute. Fight the chargebacks you do get with evidence, fast, inside the deadline.

- Layer 4: Watch the ratio. Keep your dispute rate under the card network thresholds so your processor never threatens your account.

Layer 1: Screen the Order Before You Ship

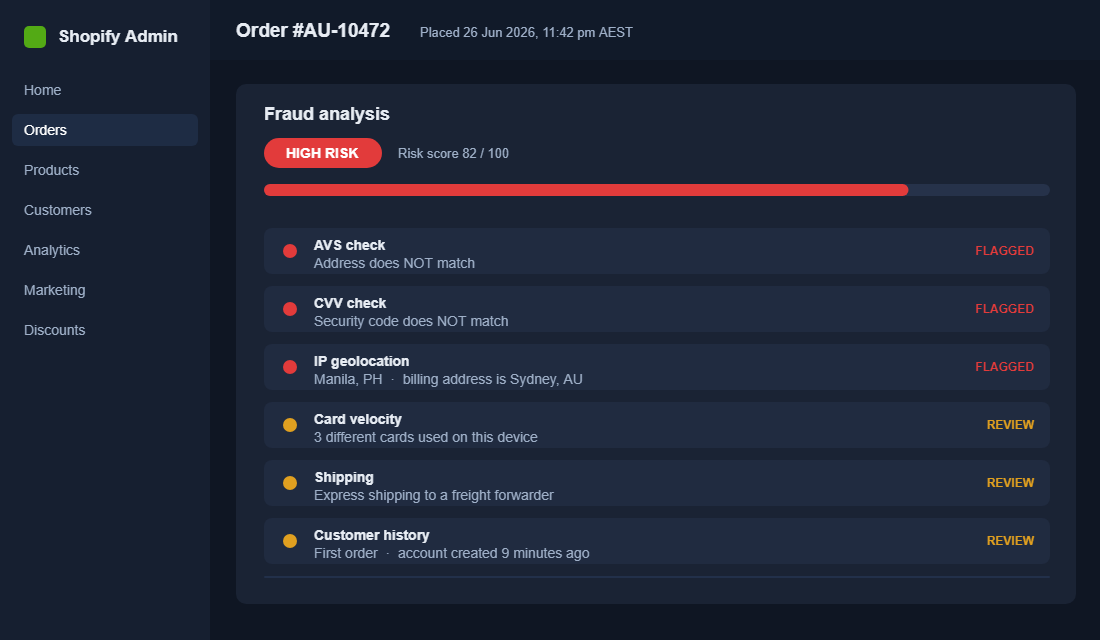

The cheapest chargeback to win is the one you never ship. Shopify already gives you a fraud analysis on every order, scoring it low, medium, or high risk based on signals like a billing address that does not match the card, multiple cards from one device, or a shipping country that does not line up with the IP.

Most founders never look at it. Build the habit instead. Before you fulfil a high-value order, open the order page and check the fraud indicators. If the AVS (address) and CVV checks both failed and the order is high risk, that is three red flags on one transaction. Hold it, and email the customer to confirm before you ship.

The signals that should make you slow down and verify:

- AVS and CVV mismatch. The card details do not match what the bank has on file.

- Express shipping on a first-time, high-value order. Fraudsters want the goods before the real cardholder notices.

- Mismatched geography. An Australian billing address, an IP in another country, and an interstate or overseas freight forwarder as the delivery point.

- Multiple failed payment attempts followed by a success, often a sign of card testing.

If you are doing real volume, manual review stops scaling. This is where guaranteed protection earns its keep. Tools like Signifyd install on Shopify in one click, score every order against a network of merchants in milliseconds, and take on the financial liability for orders they approve. If a Signifyd-approved order turns into a fraud chargeback, they pay it, not you. You trade a percentage fee for the certainty that fraud is no longer your problem to underwrite.

Layer 2: Remove the Excuse for Friendly Fraud

Since three in four disputes come from real customers, Layer 2 is where most of your money is actually leaking. People file friendly fraud for boring reasons: they did not recognise the charge on their statement, the parcel was late, the return felt too hard, or a family member bought something they forgot about. Remove the reason and you remove the dispute.

Start with your billing descriptor. That is the name that shows up on the customer’s bank statement. If your store trades as “Bondi Active” but the descriptor reads “SP NEWCO PTY LTD”, a chunk of customers will not recognise it and will call their bank instead of you. Set the descriptor in your Shopify Payments settings to your actual store name, and add your support number where the processor allows it.

Then close the gaps that breed disputes:

- Send tracking the moment you ship. A customer who can see where their parcel is does not panic and dispute. Use Australia Post or your carrier’s tracking and surface it in the shipping confirmation email.

- Make your refund and returns policy obvious. The easier you make a legitimate return, the fewer people skip you and go straight to the bank. A clean returns flow is cheaper than a chargeback every time.

- Reply to support fast. Most friendly fraud is a customer who could not reach you. A same-day reply to “where is my order” prevents the dispute that costs you four times the order value.

- Confirm delivery with proof. Signature or photo-on-delivery for high-value orders gives you the evidence you need if it ever escalates.

This layer overlaps with retention, which is the point. The same email and SMS discipline that recovers a sale also prevents a dispute. If your post-purchase communication is thin, your chargeback rate and your repeat rate both suffer. Tightening your checkout and recovery flows does double duty here.

Layer 3: Win the Disputes You Do Get

Some chargebacks will get through no matter how tight your front end is. The mistake is accepting them by default. US merchants who actually fight win an average of 54% of the chargebacks they contest. You cannot win the ones you do not respond to, and “do nothing” is a guaranteed loss plus a fee.

Speed matters more than it used to. As of July 2025, Visa tightened the response window: merchants now have 9 days in the US and Canada and 18 days in other regions to submit evidence, down from 20. Treat a dispute notification as a same-week job, not a someday job. Miss the clock and the decision is automatic.

When you respond (Shopify calls this submitting a “response” inside the dispute in your admin), the evidence that wins is specific and stacked:

- Proof of delivery. Tracking number, carrier, delivery confirmation, and where possible a signature or photo.

- The customer’s own data. IP address, device, matching billing and shipping address, and AVS or CVV match on the original order.

- The interaction trail. Order confirmation, every email and chat with the customer, and your published refund policy they agreed to at checkout.

- Usage evidence for digital or account-based products. Login timestamps or download logs that show the product was used.

If you sell at volume, fighting every dispute by hand is a job no founder should be doing. This is where you either lean on Shopify Protect (covered below) or a dedicated dispute tool that auto-assembles and submits the evidence on your behalf. Documenting the repeatable steps in a simple standard operating procedure means a VA can run the response within the deadline without you touching it.

Layer 4: Watch Your Ratio Before the Network Does

There is a number that matters more than any single dispute: your chargeback ratio, the share of your transactions that turn into disputes. Cross the card network’s line on this and the conversation stops being about individual chargebacks and starts being about whether you can keep accepting cards at all.

Visa’s updated monitoring program (VAMP) sets the bar. From June 2025, a merchant with a VAMP ratio above 2.2% is classed as “excessive”, and in North America and the EU that threshold drops to 1.5% from April 2026. Sit in the excessive band and you face fines, higher processing rates, and in the worst case a processor that drops you. For context, the broader payment card fraud rate in Australia sat at 78.8 cents per $1,000 spent in 2024, so the room between healthy and flagged is thinner than most founders assume.

Track it monthly. Divide your disputes by your total transactions and watch the trend, not just the single month. If the line is creeping toward 1%, that is your early warning to tighten Layers 1 and 2 before the network forces your hand. The founders who never get a scary email from their processor are the ones watching this number while it is still boring.

Which Orders Attract the Most Chargebacks

Not every order carries the same risk, and knowing where chargebacks cluster lets you point your effort where it pays. The pattern is consistent across Australian stores: the higher the resale value and the easier the item is to flip, the more fraud it attracts.

- High-AOV electronics and tech. Phones, cameras, and gadgets are liquid and easy to resell, which makes them a magnet for stolen-card fraud. Verify every high-risk order in this category before shipping.

- Hyped drops and limited streetwear. Sneaker and apparel releases bring a spike of new accounts, bots, and resellers. New customer plus express shipping plus a release date is a combination worth a second look.

- Subscriptions and consumables. Recurring billing breeds “I forgot I was subscribed” disputes. Clear renewal reminders and an obvious cancel path are your defence, not just a courtesy.

- Digital products and gift cards. Instant delivery means no shipping trail to use as evidence, so capture login or redemption data as your proof.

You do not need to treat a $40 order the way you treat a $900 one. Spend your manual review on the orders that would actually hurt to lose, and let your tools handle the long tail of small, low-risk transactions.

Tool Setup: Turn On Shopify Protect First

If you are on Shopify Payments, the first tool to switch on is free. Shopify Protect analyses eligible orders, fights the chargeback for you if one lands, and reimburses the order value and the dispute fee when an order is covered. It will not catch everything (it is tied to Shopify Payments and eligible orders only), but it removes a category of work for zero cost, so there is no reason to leave it off.

- Step 1. Confirm you are using Shopify Payments as your processor. Protect only covers orders processed through it.

- Step 2. In your Shopify admin, go to Settings, then Payments, and find the Fraud protection or Shopify Protect section.

- Step 3. Turn Shopify Protect on. Covered orders will show a green “Protected” badge on the order page so you know which ones are guaranteed.

- Step 4. For anything Protect does not cover (other processors, ineligible orders, higher fraud exposure), layer a guaranteed-protection app like Signifyd over the top so nothing falls through the gap.

The principle is simple: free native protection first, paid guaranteed protection for the exposure that is left. You are not choosing one tool. You are stacking them so the cheap one carries the easy cases and the paid one carries the risk you cannot afford to underwrite yourself.

The Compound Effect: How the Four Layers Work as One

Any single layer on its own is leaky. Screening alone does nothing for friendly fraud. Great post-purchase comms still let the occasional stolen card through. Winning disputes is reactive, and watching your ratio only tells you the damage after it is done. The power is in the stack.

Run all four and the maths compounds in your favour. Layer 1 removes the fraud orders. Layer 2 removes most of the friendly-fraud excuses. Layer 3 wins back half of what still slips through. Layer 4 keeps you safely under the thresholds that put your whole account at risk. The store next to you, fighting nothing and watching nothing, is paying $4 for every $1 of fraud and slowly drifting toward an excessive ratio. You are not.

There is a retention payoff too. Every Layer 2 habit (fast support, clear tracking, easy returns) is the same behaviour that turns a first-time buyer into a repeat customer. Protecting your margin and growing your customer lifetime value are the same project wearing two hats.

Your Chargeback Defence Checklist

Work through this once to set up the system, then revisit Layer 4 every month. Copy it into a doc and tick it off:

- Layer 1. Check Shopify’s fraud analysis on every high-value order. Hold and verify anything high risk with AVS or CVV mismatch. Add guaranteed screening (Signifyd) if you are past manual-review volume.

- Layer 2. Set your billing descriptor to your trading name. Send tracking automatically. Make returns easy and reply to support same-day. Use proof of delivery on high-value orders.

- Layer 3. Never auto-accept a dispute. Respond inside the 9 or 18 day window with delivery proof, customer data, and the full interaction trail. Write an SOP so a VA can run it.

- Layer 4. Calculate your chargeback ratio monthly. Keep it well under 1%. Act the moment it trends up, not when the processor emails you.

- Tools. Turn on Shopify Protect today if you use Shopify Payments. Layer a guaranteed-protection app over the exposure it does not cover.

Inside eCommerce Circle, Protection is one of the core pillars we work on with every member, because nothing kills a healthy-looking store faster than margin leaking out the back through fraud and disputes. If you want a second opinion on your chargeback exposure, let’s talk.