On 1 October 2026, the RBA bans surcharging on Visa, Mastercard, and eftpos credit and debit cards. Every Aussie Shopify founder who has been quietly passing on processing fees to customers is about to lose that lever overnight. The fee does not disappear. The customer just stops paying it. You do.

What’s in This Article

If your store does $2 million a year and you have been surcharging at an average 1.1%, that is $22,000 of margin moving from the customer’s column to yours on 1 October. For a 22% contribution-margin brand, that is more than two months of net profit gone in a single regulatory change.

The good news: most Aussie Shopify stores have 0.4 to 1.2 percentage points of processing margin sitting in plain sight that they have never audited. Wrong Shopify plan for their volume. Lazy method-mix that defaults to the highest-fee BNPL option. Failed payment flows that silently leak 1 to 3% of revenue. Chargeback fees treated as cost of doing business when half of them are recoverable. This article is the 6-lever audit Aussie DTC founders run before October to find that margin and bank it before the ban lands.

Lever 1: Audit Your True Effective Processing Rate

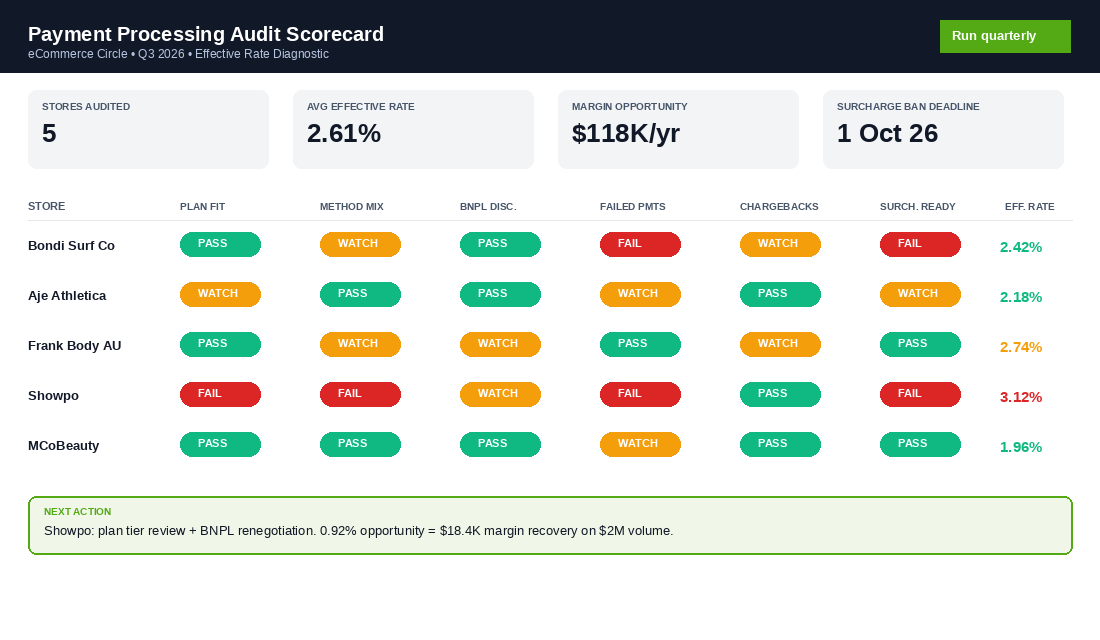

The number that matters is not the rate on the Shopify pricing page. It is your effective rate: total processing fees paid divided by gross processing volume across every method (card, Shop Pay, Apple Pay, Google Pay, PayPal, Afterpay, Klarna, Zip). Most Aussie founders we work with cannot quote this number to within 0.3% when asked. That is the first problem.

The formula is simple, but the data has to come from three places at once:

- Shopify Payments payouts. Shopify Admin, Finances, Payouts, Export. Pull the last 12 months. Each payout row shows gross, fees, and net.

- Third-party processor reports. PayPal, Afterpay, Klarna, Zip, Stripe each have their own monthly statement. Download all of them.

- Shopify third-party fee. If you use anything other than Shopify Payments as the processor, Shopify adds a 2.0% (Basic), 1.0% (Grow), or 0.6% (Advanced) third-party transaction fee. This shows up on your Shopify subscription invoice, not the processor statement.

Sum the fees, divide by gross processed volume, and you have your true effective rate. A healthy Aussie Shopify store on Shopify Payments with a reasonable method mix sits at 1.95% to 2.35% effective. A store leaking margin sits at 2.6% to 3.4%. Anything above that and you have a method-mix or plan-mismatch problem, not a rate problem.

The audit dashboard below is the one we build with every brand in eCommerce Circle. Three months of Shopify and processor data in, an effective rate per channel out, with the gap to the brand-wide target colour-coded so you know where to dig first.

Lever 2: Match Your Shopify Plan to Your True Volume

Shopify Payments processing rates in Australia in 2026:

- Basic. 1.6% + 30c domestic online, 2.9% + 30c international or Amex.

- Grow (formerly Shopify). 1.6% + 30c domestic online (same rate, lower third-party fee).

- Advanced. 1.4% + 30c domestic online, 2.9% + 30c international or Amex.

- Plus. Negotiated, typically 1.2% + 30c domestic, with volume tiering below that for stores processing $5M+ a year.

The Advanced break-even versus Basic is the most common miscalculation. The Advanced plan costs roughly $390 AUD more per month than Basic but saves 0.2% on every domestic transaction. At $200K a month in card volume, that is $400 of fee savings against $390 of extra subscription cost. Advanced pays for itself at $195K/month and starts compounding hard above $300K/month.

The Plus break-even is harder because the merchant rate is negotiated, but a 1.2% rate against Advanced’s 1.4% is 0.2% across all volume. At $500K/month, that is $1,000 of monthly savings before you factor in any Plus-specific features (Shopify Functions, B2B, multi-store, custom checkout). Most Plus discussions get framed around features. The cleaner version is to frame the conversation around processing margin first, features second.

Pull your last six months of monthly Shopify Payments volume, run the break-even on every plan tier above your current one, and either commit to the upgrade or kill the conversation for another quarter. We see two stores a quarter sitting on Basic at $250K/month when Advanced is the obvious move. That is $6K a year of margin that walks out the door.

Lever 3: Method-Mix Optimisation (the Real Margin Lever)

Plan tier moves the needle 0.2 to 0.3%. Method mix moves it 0.5 to 1.5%. The question is not which methods to offer, it is in what order and with what prominence.

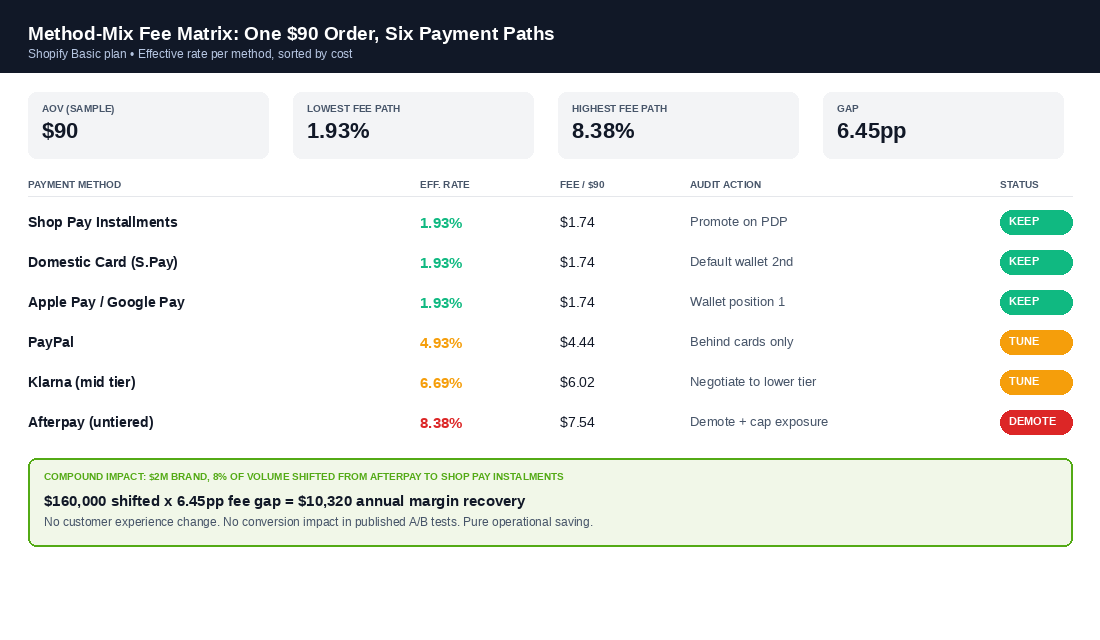

Here is the real fee stack for a typical $90 Aussie order:

- Shopify Payments domestic card (Basic plan): 1.6% + 30c = $1.74 = 1.93% effective.

- Shop Pay Installments / Apple Pay / Google Pay over Shopify Payments: same as card, 1.93%.

- PayPal: 2.6% + 30c = $2.64 = 2.93% effective. Plus 2.0% Shopify third-party fee on Basic = 4.93% all-in.

- Afterpay: 5.6% to 6.5% + 30c. Centre of band on a $90 order is $5.74 = 6.38%. Add 2.0% Shopify third-party fee = 8.38% all-in.

- Klarna: 3.29% to 5.99% + 30c. Usually negotiated at a tier-banded volume rate. Centre is around 4.69% + 30c. Add Shopify third-party fee.

- Zip: Similar to Afterpay, 4% to 6% range depending on negotiated tier.

The headline: Afterpay on a Shopify Basic plan costs you 4.5x more per dollar processed than card. That is fine if Afterpay’s incremental conversion lift is genuinely 4.5x its fee delta. It rarely is. Afterpay attaches in 8 to 22% of Aussie DTC checkouts depending on category, and the incremental conversion lift on stores that test it has historically landed at 12 to 20%, not 350%.

The method-mix optimisation is not “remove Afterpay”. It is “stop defaulting to Afterpay”. Three concrete moves:

- Push Shop Pay Installments above Afterpay in your wallet order. Shop Pay Installments charges the merchant the same as a regular card transaction in most cases. Customer still gets four interest-free instalments. You save 4 to 5 percentage points on every order that switches.

- PDP messaging discipline. Most Aussie stores still have Afterpay’s “Or 4 payments of $22.50” widget hard-coded above Shop Pay Installments. Reverse the order or remove the Afterpay widget on PDPs above a certain AOV. The fee impact is meaningful.

- Cart and checkout placement. If you cannot remove Afterpay, at least demote it. Wallet buttons (Apple Pay, Google Pay, Shop Pay) sit first. Card sits second. BNPL options sit below the fold or in an expand-on-click section. We have seen this single change shift BNPL share of orders from 22% down to 14% with no measurable change in overall conversion.

Lever 4: BNPL Discipline (Negotiate, Tier, and Cap)

If you are processing more than $20K a month through Afterpay, Klarna, or Zip, your rate is negotiable. Volume-tier rates exist for every BNPL provider in Australia, but they are not advertised. You have to ask. Three things to push for:

- Tiered rate by monthly volume. A common Afterpay structure is 6.0% under $50K/month, 5.4% from $50K to $200K, and 4.8% above $200K. If you are at $80K/month and still paying 6%, you are leaving 0.6% on the table.

- Promo card and partnership credits. Most BNPL providers run quarterly merchant promotions where they fund 5 to 15% co-op marketing. If you spend that, you recover 0.3 to 0.5% effective. Ask for the latest co-marketing terms when you renegotiate.

- Settlement timing. Some BNPL providers settle T+2 by default but offer T+1 for an extra 0.1% (or T+0 for 0.2%). For most Aussie stores running $80K to $200K/month, the working-capital benefit of T+1 versus T+0 is not worth the fee. Default to the cheaper settlement window unless you are cashflow-tight (see the cash conversion cycle playbook for how to think about that trade-off).

The second BNPL discipline issue is AOV cannibalisation. Afterpay’s average order value lift is real (Afterpay’s own data shows 15 to 30% AOV lift on attached orders), but a slice of that uplift is fee-eaten margin. On a $90 order with 22% contribution margin, you keep $19.80. The same $90 order on Afterpay drops your fee from 1.93% to 8.38% all-in. Margin drops from $19.80 to $14.00. If the Afterpay attach was a forced choice (customer would have bought anyway on card), the lift evaporates.

Run a quarterly cannibalisation test: pull a 30-day window of orders, split Afterpay from card, compare same-customer second-purchase rates 90 days later. If your Afterpay-acquired customers repeat at a similar rate to card customers, you are paying for genuine incremental volume. If they repeat at 30 to 50% less, you are subsidising customers you would have got anyway.

Lever 5: Failed Payment and Retry Engineering

Most Aussie Shopify founders have never looked at their failed payment rate. The number sits inside Shopify Admin under Analytics, Reports, Checkout, but it is not on the standard dashboards. A normal failed payment rate for an Aussie Shopify store is 1.8 to 3.2%. A leaking store sits at 4 to 7%.

A failed payment is not always a customer who walks away. About 35 to 45% of failed payments are recoverable with a soft retry, a different funding method, or a network re-route. The recoveries that nobody asks for are the cheapest revenue on the internet.

The four-step retry engineering Aussie brands should run:

- Klaviyo or Shopify abandoned checkout email at T+30 minutes. Subject line “Your order didn’t go through, here is a one-click link to try again.” This catches 8 to 14% of failed payments.

- SMS at T+2 hours. Twilio or Klaviyo SMS, single line: “Hi {first}, the card on your order $X didn’t process. Tap to retry: {link}”. SMS recovers another 4 to 8%.

- Manual review of “do not honor” responses. About 12% of declined transactions are “do not honor” responses, which usually mean the bank flagged the merchant or the velocity, not the card. Pulling these into a daily review queue and reaching out personally recovers around 35% of them on stores doing $80K+/month.

- Network re-routing on Shopify Payments. Shopify Payments now offers automatic retry on a different processing rail for certain decline codes. This is on by default for most Shopify Plus stores and off for Basic/Advanced unless requested. Ask your account manager (Plus) or Shopify Support (Basic/Advanced) to enable it.

A $2M brand with a 2.8% failed payment rate and a 0% recovery program is leaving roughly $11K to $19K of recoverable revenue on the floor every year. On 22% contribution margin, that is $2,400 to $4,200 of pure margin. Setup time for the Klaviyo flow and SMS is two hours.

Lever 6: Chargeback Cost Recovery

Every chargeback on Shopify Payments costs you $15 USD in dispute fee plus the lost merchandise plus the original transaction fee. Even if you win the dispute. The win does not refund the $15 dispute fee, only the disputed transaction amount.

For a brand doing 23,000 orders a year with a 0.6% chargeback rate (138 chargebacks), that is $2,070 USD just in dispute fees. Plus the merchandise and shipping on the ones you do not win, which is typically 55 to 70% of disputes for unprepared merchants.

Three lever moves on the chargeback line:

- Block obvious fraud before it processes. Shopify’s built-in fraud filter is decent but conservative. Stores doing $80K+/month should layer on NoFraud, Signifyd, or Riskified for high-risk orders. Cost is $0.05 to $0.25 per screened order with a fraud-cover guarantee. Cuts fraudulent chargebacks 60 to 80%.

- Improve evidence packs. Most Aussie stores submit dispute evidence as a generic order confirmation. Win rates on that approach are 25 to 35%. Stores that submit structured evidence packs (tracking, signed delivery, IP/device match, customer comms timeline) win 55 to 70%. Templated evidence packs through Disputifier, Chargeflow, or Justt run $20 to $50 per dispute or 25% of recovered revenue.

- Friendly-fraud-aware response queue. “Item not received” disputes (the biggest single category of friendly fraud) need a different evidence pack than fraud disputes. Photo-on-delivery, signature-on-delivery for orders above $150, and AusPost MyPost Business proof-of-delivery should be the default on every shipment above your AOV.

The full chargeback and return-abuse defence is its own playbook (see the return abuse defence playbook for the operational detail). The processing-fee angle: a brand that drops its chargeback rate from 0.7% to 0.3% on $2M of volume recovers around $11K of avoided fees, lost merchandise, and dispute-fee leakage per year.

The Compound Effect: What This Adds Up to on a M Aussie Shopify Store

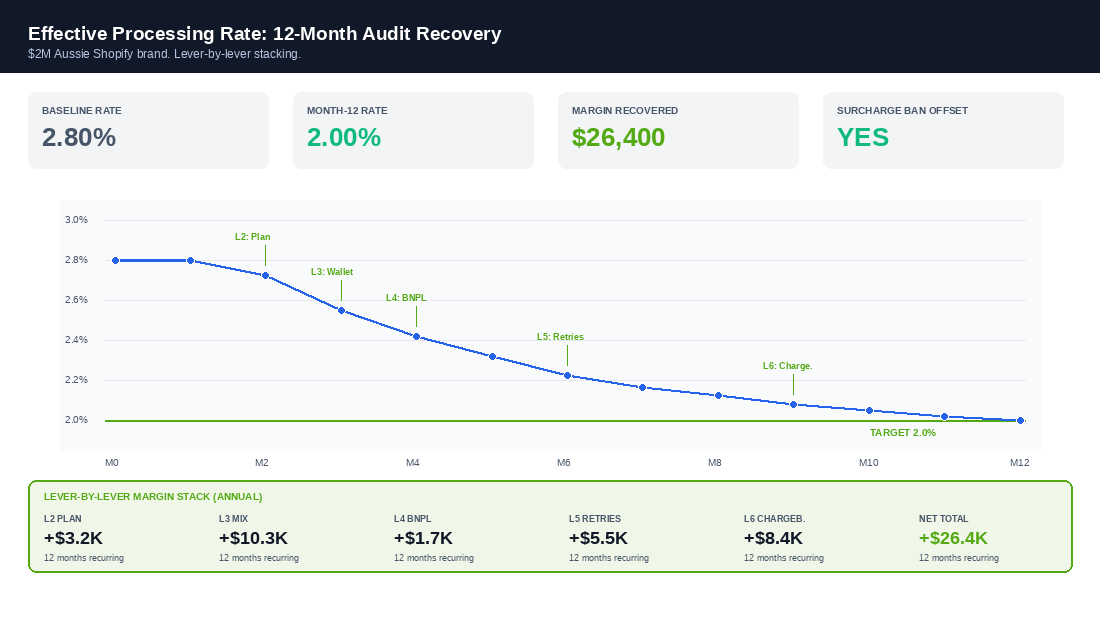

Let’s stack the levers on a representative Aussie brand: $2M gross volume, 23,500 orders at $85 AOV, currently sitting at a 2.8% effective processing rate.

- Lever 1 (audit and dashboard). Zero direct saving. Surfaces the gap so the rest of the levers can be priced.

- Lever 2 (plan upgrade Basic to Advanced). 0.2% saving on $1.6M of domestic volume = $3,200/year less the $4,680/year subscription delta. Net at scale: break-even now, accretive at $300K+/month.

- Lever 3 (method-mix, demote Afterpay 22% to 14% share). 8% of $2M shifted from 8.4% to 1.93% effective = $440 saving per $1K of shifted volume. On $160K of shifted volume: $10,300/year.

- Lever 4 (BNPL renegotiation 6.0% to 5.4%). 0.6% on remaining $280K of BNPL = $1,680/year.

- Lever 5 (failed payment recovery, 0% to 45% recovery). 2.8% fail rate, 45% recovery = $25K recovered revenue at 22% margin = $5,500/year.

- Lever 6 (chargeback rate 0.6% to 0.3%, win rate 30% to 65%). Avoided fees, merchandise, and dispute leakage = $8,400/year.

Add the surcharging-ban context. The brand has been collecting 1.1% surcharge on 70% of orders = $15,400/year in revenue that was passed through to absorb processing fees. From 1 October 2026, that revenue line goes to zero. The brand needs to recover at least that much from the other side to stay flat on margin.

The six levers above stack to roughly $26K to $30K of recovered margin annually on a $2M brand, which is the gap. The surcharge ban is not a margin event for a brand that has run this audit. It is a margin event for everyone who has not. See the contribution margin audit playbook for how to feed this into your full unit economics and the CAC payback period playbook for what 80 basis points of recovered margin does to your acquisition headroom.

The Hidden Seventh Lever: International Cards and Currency Conversion

The six levers above cover domestic volume. If more than 10% of your orders come from overseas cards, there is a seventh leak worth auditing before October: international card fees and currency conversion.

Here is the stack on a typical international order through Shopify Payments in Australia. The international card rate is 2.9% + 30c on Basic and Advanced, against 1.6% domestic. That is a 1.3 point premium before anything else happens. If you sell in local currencies through Shopify Markets, Shopify adds a 1.5% currency conversion fee on top of processing. And if your payout currency does not match your selling currency, you wear a second conversion on the way out.

- Measure the international share first. Export 90 days of orders and split them by card country. A store with 18% international volume at 2.9% is carrying a blended premium of roughly 0.23 points across the whole book without ever seeing it on a statement.

- Decide whether local-currency selling pays for itself. Shopify’s own Markets data puts the conversion lift from local-currency pricing at 10 to 25% in most markets, which usually beats the 1.5% conversion fee on contribution margin. Run the maths per market, not globally, and price each market deliberately (the pricing power playbook covers how to set those points without racing to the bottom).

- Watch the Amex line. Amex routes at the higher rate even for domestic Aussie cards on most plans. If Amex is more than 6 to 8% of your volume it quietly drags the blended rate up. Do not remove it, because Amex AOVs typically run 20 to 40% higher, but price its drag into your effective rate target.

A $2M brand with a 15% international mix can typically claw back $2K to $5K a year by aligning payout currency, letting Markets price in local currency where the lift covers the fee, and treating Amex as its own line in the lever 1 dashboard rather than averaging it away.

The 30-Day Audit Sprint

You have four months between now and the 1 October surcharging ban. A 30-day sprint to get the six levers in place looks like this:

- Week 1 (Days 1 to 7): Data pull and effective rate calc. Pull 12 months of Shopify payouts and every third-party processor statement. Build the dashboard. Land on your current effective rate to 0.05%.

- Week 2 (Days 8 to 14): Plan and method mix. Run the Advanced and Plus break-evens. Reorder the wallet buttons in your checkout. Demote BNPL widgets on PDPs above your AOV.

- Week 3 (Days 15 to 21): BNPL renegotiation and failed payment flows. Get on a call with Afterpay, Klarna, and Zip account managers. Push for a tier rate. Set up the Klaviyo and SMS failed-payment recovery flows.

- Week 4 (Days 22 to 30): Chargeback hardening. Install or upgrade fraud screening. Stand up the structured evidence pack template. Switch high-AOV orders to signature-on-delivery.

Run the audit again on Day 60. The effective rate should have dropped 0.4 to 0.8 percentage points. The remaining 0.4 to 0.6 points come from the slower-burn levers (chargeback rate dropping, failed payment recoveries compounding) over months three to six.

The Three Failure Modes That Eat the Recovery

We have walked dozens of Aussie founders through this audit. Three patterns destroy the margin gain if you let them:

- Treating the audit as a one-off. Method mix drifts every quarter as new payment apps push themselves up the wallet stack. Re-run lever 3 quarterly or you lose 0.2% to creep.

- Skipping the BNPL renegotiation because it feels awkward. Every BNPL provider expects renegotiation conversations at $50K, $100K, $200K, and $500K monthly volumes. Asking is not rude. Not asking is a 0.6% gift.

- Removing surcharging without telling your customer base. If you have been visibly surcharging 1.1% and you remove it silently, you have effectively given a 1.1% discount with no marketing payoff. Communicate the change. “From 1 October, we have absorbed card processing fees so the price you see is the price you pay” is a brand-trust moment, not a cost line.

The Bigger Picture

Payment processing margin is the most ignored profit lever in Aussie DTC. Founders will obsess for weeks over a 0.3% conversion test that might land or might not. Meanwhile a 0.8% processing audit that compounds across every single order goes untouched for years. The 1 October surcharging ban is the deadline that forces the issue. If you run the six levers between now and September, you walk into Q4 with 60 to 100 basis points of structural margin recovered. If you do not, you walk into Q4 with $20K to $40K of margin quietly bleeding because the surcharge line stopped covering it.

Inside eCommerce Circle, the processing-fee audit is one of the first three financial-system reviews we run with every new member. If you want a second pair of eyes on yours before October, let’s talk.