You packed the order. You shipped it. You can see the delivery confirmation sitting in your Australia Post dashboard. Then six weeks later the money vanishes from your payout, a dispute fee lands on top, and you are suddenly arguing with a bank about a parcel you know arrived.

What’s in This Article

That is the chargeback experience for most Aussie Shopify founders: reactive, confusing, and quietly expensive. Most treat disputes as a cost of doing business. They fire off a half-finished response inside Shopify, lose, and move on. The brands that protect their P&L treat chargebacks the way they treat conversion: as a system with inputs they control.

The numbers say this is worth your attention. Card-not-present fraud on Australian-issued cards jumped 19% to $816 million in 2024, and it now makes up 90% of all card fraud in the country, according to AusPayNet. Globally, chargebacks cost ecommerce merchants an estimated $33.79 billion in 2025. And here is the kicker: Visa estimates up to 75% of chargebacks are not criminals at all. They are your own customers disputing legitimate purchases, a problem the industry politely calls friendly fraud.

This playbook gives you the 6-layer defence system we work through with eCommerce Circle members: screen, prevent, deflect, fight, automate, monitor. Work through it once and chargebacks stop being a random tax and start being a managed metric.

Why a Chargeback Hurts Four Times More Than a Refund

A refund costs you the sale. A chargeback costs you the sale, the product, the original shipping, the payment processing fees you do not get back, and a dispute fee from your processor (typically 15 to 25 dollars, which Shopify Payments returns only if you win). Stack on the staff time to respond and research from LexisNexis puts the all-in cost at roughly $4.61 for every dollar of fraud. Other industry studies land the average total cost of a single dispute near $110 once you count everything.

So a $90 chargeback is never a $90 problem. And the damage is not only financial.

Card networks track your dispute ratio: chargebacks divided by transactions. Visa’s monitoring programs start paying attention around 0.65%, and merchants who climb toward 1% land in formal monitoring with fines and, in the worst case, the loss of card processing entirely. For a Shopify store, that can mean losing Shopify Payments. Your dispute ratio is an asset you defend, the same way you defend your sender reputation in email.

One more piece of context before the layers. Disputes arrive under reason codes, and the code dictates your defence. Three buckets matter:

- True fraud. A stolen card was used. The real cardholder disputes it. Your defence is stopping these orders before fulfilment, because once the parcel ships you will almost certainly lose.

- Friendly fraud. The genuine customer bought the item, then disputed it anyway. Forgot the purchase, did not recognise your name on the statement, wanted a refund without talking to you, or a family member ordered it. This is up to three quarters of all disputes and it is highly winnable.

- Merchant error. Wrong item, duplicate billing, subscription that kept charging. These are on you. Fix the process, refund fast, do not fight.

Layer 1: Screen Every Order Before It Ships

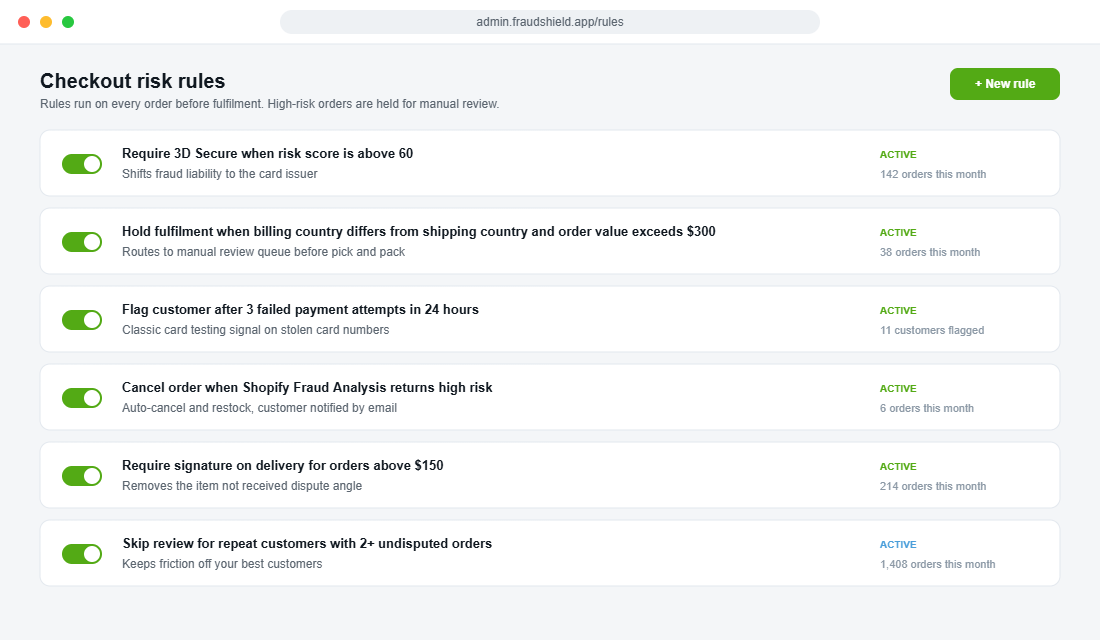

True fraud is won or lost at fulfilment. Once a parcel bought on a stolen card leaves your 3PL, the chargeback is coming and no evidence pack will save you. So the first layer is a screening gate between “order paid” and “order picked”.

Shopify already does the heavy lifting. Every order gets a fraud analysis with risk indicators: does the billing address match the card, did the CVV pass, how many payment attempts were made, does the IP location line up with the shipping address. Most founders never look at it until after they have been burned. Flip that. Make the risk check part of your daily fulfilment routine, or better, automate it.

The patterns worth a hard look are consistent across every store we coach:

- Billing country and shipping country do not match on a first-time order above a few hundred dollars.

- Multiple failed payment attempts before a success. This is card testing: someone working through a list of stolen numbers.

- Express shipping on a high-value first order with a free email domain and a phone number that does not answer. Fraudsters want the goods moving before the cardholder notices.

- Mismatched names across the card, the email, and the delivery address with no gift note.

Two settings do most of the work. First, turn on 3D Secure for risky orders. When a transaction is authenticated with 3DS, liability for fraud generally shifts to the card issuer, not you. Shopify Payments supports this natively. Second, hold high-risk orders for manual review. A 30-minute review queue each morning costs you almost nothing; shipping one fraudulent $400 order costs you the product, the shipping, and a near-certain loss.

The discipline cuts both ways: build a fast lane too. A repeat customer with two or more clean orders should never sit in a review queue. Friction belongs on risk, not on loyalty.

Layer 2: Close the Friendly Fraud Gaps

If 75% of disputes come from real customers, then most chargeback prevention is actually customer experience work. Every friendly fraud dispute starts with a moment of confusion or frustration that was cheaper to send to the bank than to you. Your job is to remove those moments.

- Fix your billing descriptor. If your store is Coastal Threads but the card statement says your holding company, you will collect “I do not recognise this charge” disputes forever. Set the statement descriptor in your payment settings to the brand name customers actually bought from.

- Confirm everything in writing. Order confirmation, shipping confirmation with live tracking, delivery confirmation. Customers who can see where their parcel is do not file “item not received” disputes. Merchants using automated shipping notifications consistently report fewer delivery disputes.

- Require a signature above a threshold. Somewhere around 150 dollars, switch off Authority to Leave and require a signature. A signed delivery is the single strongest piece of evidence against an “item not received” claim.

- Make support easier to find than the bank’s dispute button. Contact link in every transactional email, response time under 24 hours, and a returns process that does not feel like a fight. A refund you grant costs you the sale. A dispute you lose costs four times that.

- If you sell subscriptions, over-communicate. Send a reminder before each renewal and put a working cancel link in every email. “Cancelled subscription kept charging” is one of the most common dispute reasons on Shopify subscription brands, and it is entirely preventable.

This layer pairs with your returns experience. We covered the abuse side in the Return Abuse Defence Playbook, but the principle here is the inverse: make the legitimate path so easy that the bank is never the path of least resistance.

Layer 3: Deflect Disputes Before They Become Chargebacks

Between “customer calls their bank” and “chargeback lands in your Shopify admin” there is a short window where the dispute can be intercepted. The card networks built tooling for exactly this, and most Aussie founders have never heard of it.

Verifi (Visa) and Ethoca (Mastercard) run alert networks that ping you when a cardholder starts a dispute. You typically get 24 to 72 hours to act. Refund the order inside that window and the dispute never becomes a chargeback: no fee, no hit to your dispute ratio, no black mark with the network. Chargeback apps like Chargeflow and Disputifier plug these alerts straight into Shopify, so the refund-or-fight decision happens in one place.

The decision rule we give members is blunt maths. If the order value is under your all-in dispute cost (call it 110 dollars) and the evidence is thin, refund on alert and keep your ratio clean. If the order is high value and your evidence is strong, let it proceed and fight it properly in Layer 4. What you never do is ignore the alert and let a winnable dispute become a formal chargeback by default.

Visa also runs Order Insight, which lets participating merchants push order details (item, delivery address, device used) straight into the bank’s app when a cardholder taps “I do not recognise this charge”. A surprising number of disputes die right there, when the customer sees their own purchase history staring back at them.

Layer 4: Fight Back With Evidence That Actually Wins

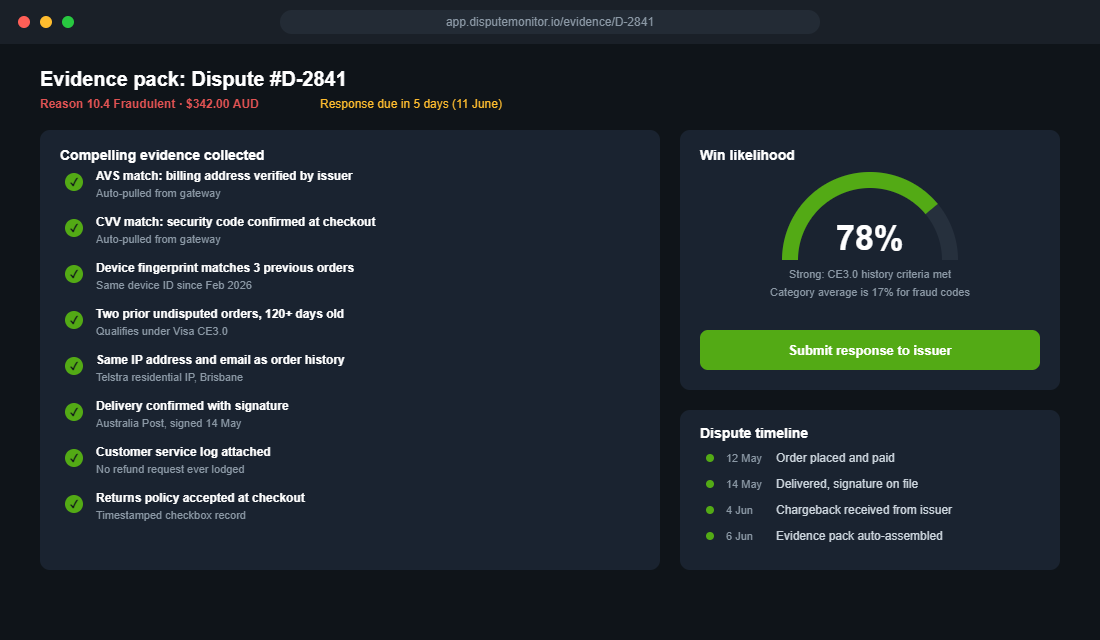

Here is the statistic that should change how you respond to disputes: merchants who fight chargebacks with structured evidence win around 54% of the cases they contest. Merchants who fire off a default response to fraud-coded disputes win about 17%. Same dispute, wildly different outcome. The difference is the evidence pack.

Since Visa’s Compelling Evidence 3.0 rules rolled out (with major automation enhancements landing in late 2025), the playbook for friendly fraud got dramatically better for merchants. Under CE3.0, if you can show two prior undisputed transactions from the same customer, older than 120 days, matching on identifiers like IP address, device ID, or account login, you can shift liability for a “fraud” dispute back to the issuer. In plain English: a repeat customer claiming they never bought from you is now a fight you should win.

Your standing evidence pack, assembled for every contested dispute:

- Gateway proof. AVS match, CVV match, 3DS authentication result. Pulled from your payment provider.

- Customer history. Prior undisputed orders with dates, IP addresses, and device identifiers. This is your CE3.0 ammunition.

- Delivery proof. Tracking number, carrier confirmation, signature if you required one, and a map pin if the carrier provides it.

- Communication log. Every email, chat, and SMS with the customer. Especially anything showing they used the product or never raised an issue.

- Policy acceptance. Timestamped record that they ticked your returns and terms checkbox at checkout.

Two execution rules. Respond inside the deadline (often as short as 7 to 21 days, and the clock starts when the dispute is lodged, not when you notice it). And match the evidence to the reason code: delivery proof wins “item not received”, order history wins “fraudulent”, and nothing wins “merchant error” so do not waste hours on disputes you caused.

Layer 5: Automate the Whole System

Everything above can be done manually, and at a handful of disputes a month, it should be. Past that point the maths flips: founders do not respond to disputes at 11pm during BFCM week, and every missed deadline is an automatic loss. This is where the chargeback apps earn their keep.

Our pick for most Shopify stores: Chargeflow. It is success-fee based (you pay a percentage of recovered revenue only when a dispute is won), which makes it a sensible first move because there is no fixed cost to trial it. Setup takes about 15 minutes:

- Install Chargeflow from the Shopify App Store and approve the permissions for orders and disputes.

- Connect every payment provider you use: Shopify Payments, PayPal, and Stripe if it is in your stack. Disputes from all of them flow into one dashboard.

- Switch on chargeback alerts (the Verifi and Ethoca integration from Layer 3) and set your auto-refund threshold for low-value, thin-evidence alerts.

- Enable automated representment so every dispute gets a full evidence pack assembled from your Shopify data, formatted to the reason code and CE3.0 requirements.

- Set a weekly 10-minute review: check the dashboard, scan reason codes for new patterns, and feed anything systemic back into Layers 1 and 2.

The results from automation are not subtle. Sports merchandise giant Fanatics moved its dispute operations to Chargeflow and recovered more than 800,000 dollars in disputed revenue within months while more than doubling its win rate. If you would rather eliminate fraud risk entirely than fight disputes, Signifyd takes the opposite approach: it approves orders with a financial guarantee and eats the fraud chargebacks itself. Fashion retailer BHFO used it to push order approvals to 99.66% while cutting its chargeback rate by 69%. Disputifier sits in the middle and is strong on “item not received” prevention via shipping notifications.

Whichever tool you choose, the principle is the same: deadlines never get missed, evidence never gets forgotten, and your time goes back into growth.

Layer 6: Watch Your Dispute Ratio Like a Board Metric

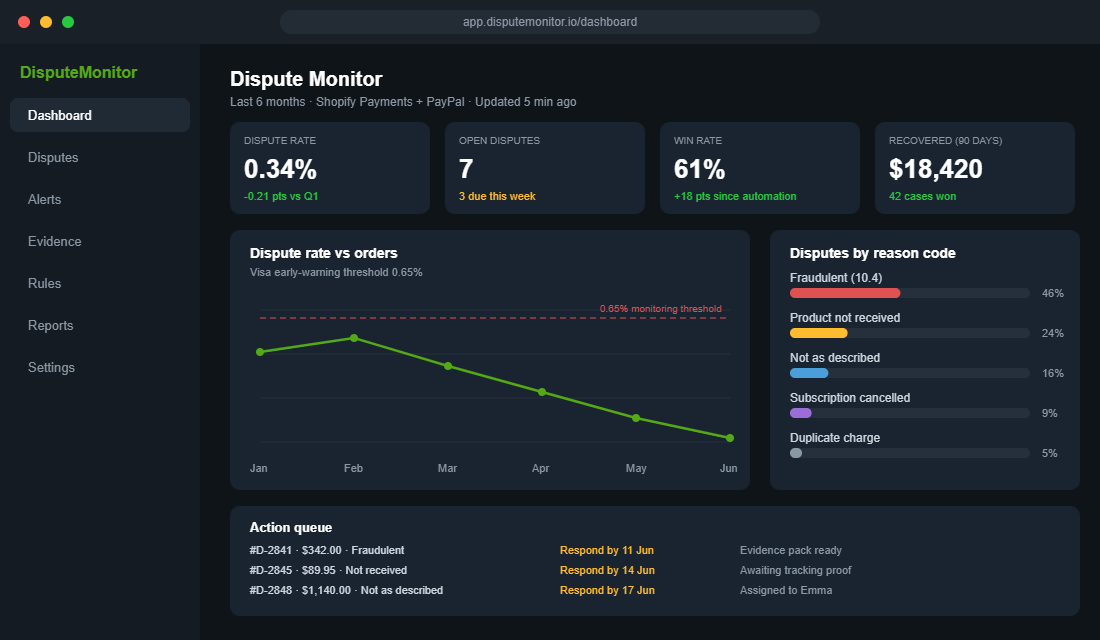

The last layer is the one that keeps the other five honest. Put four numbers on your weekly dashboard next to revenue and ROAS: dispute count, dispute ratio, win rate, and recovered dollars.

The ratio is the one with teeth. Under 0.3% means your system is working. Drifting past 0.5% means something upstream broke: a new traffic source bringing card testers, a delivery partner losing parcels, a subscription flow confusing people. At 0.65% you are inside Visa’s early warning territory and the fix becomes urgent. The reason-code mix tells you which layer to tighten: a spike in “fraudulent” points at Layer 1 screening, a spike in “not received” points at Layer 2 delivery proof.

Review the rules quarterly, and pressure-test the whole system before peak season. BFCM and the EOFY sale period bring more orders, more first-time customers, and more fraud attempts, all at the exact moment you have the least spare attention. While you are at it, this monitoring habit sits naturally alongside the quarterly fee check from the Payment Processing Audit and the security hygiene in the Shopify Admin Lockdown Playbook. Protection compounds.

How the Six Layers Compound

No single layer is dramatic on its own. Together they change the economics of every dispute that touches your store. Screening stops the unwinnable fraud orders before they ship. The friendly fraud fixes remove the confusion that creates most disputes in the first place. Alerts catch half of what remains and convert it into cheap refunds. Representment wins the majority of what you choose to fight. Automation makes all of it run without you. Monitoring tells you the moment anything drifts.

Stores that run the full stack typically cut net chargeback losses by half or better, and just as importantly, they stop carrying the low-grade anxiety of an unmanaged risk. Your dispute ratio becomes a number you control, not a number that happens to you.

The Chargeback Defence Checklist

Work through this once, then review it quarterly. Each item maps to a layer above.

- Screen: Shopify fraud analysis checked before every fulfilment run. 3D Secure on for high-risk orders. Manual review hold for risk flags. Fast lane for repeat customers.

- Prevent: Billing descriptor matches your brand name. Tracking emails on every order. Signature required above 150 dollars. Support link in every email with sub-24-hour replies. Renewal reminders and a working cancel link on every subscription email.

- Deflect: Verifi and Ethoca alerts connected. Auto-refund rule for low-value, thin-evidence alerts. Fight rule for high-value, strong-evidence cases.

- Fight: Standing evidence pack template covering gateway proof, CE3.0 order history, delivery proof, comms log, and policy acceptance. Every response inside deadline, matched to the reason code.

- Automate: Chargeback app installed, all gateways connected, automated representment on, weekly 10-minute dashboard review booked.

- Monitor: Dispute count, ratio, win rate, and recovered dollars on the weekly dashboard. Action triggers set at 0.3% and 0.5%. Quarterly rule review, plus a pre-BFCM pressure test.

Inside eCommerce Circle, Protection is one of the 10 P’s we work on with every member, and chargebacks are usually the fastest win in the pillar: a few hours of setup that pays for itself on the first dispute you deflect. If you want a second opinion on your dispute numbers, let’s talk.