Walk through the checkout of almost any Aussie Shopify store and you will find the same row of logos: Afterpay, Zip, maybe PayPal Pay in 4. Most founders switched them on years ago, watched a few orders come through, and never thought about them again.

What’s in This Article

Here is the problem with that. Every BNPL order is costing you roughly two to three times what a card payment costs. Afterpay merchant fees in Australia typically run 4 to 6% plus 30 cents per transaction, against 1 to 3% for standard card processing. If you run a 20% net margin, a 6% payment fee is swallowing close to a third of your profit on every BNPL order.

And yet ripping it out can be just as expensive. Finder’s tracking shows 41% of Australians used a BNPL service in the six months to March 2026, and PYMNTS research from 2025 found 43% of consumers will abandon a purchase entirely if BNPL is not offered at checkout. So the real question is not “should I offer Afterpay?” It is “do I actually know what BNPL is doing to my numbers?” Most founders we work with cannot answer that. This playbook fixes it.

What BNPL Actually Costs You (The Maths Most Founders Skip)

Let’s make this concrete. Take a typical order of 120 dollars on a store doing 80k a month.

- Card via Shopify Payments: around 1.75% plus 30 cents. Cost: roughly 2.40.

- Afterpay: at a 5% rate plus 30 cents. Cost: roughly 6.30.

- The gap: close to 4 dollars per order. If 15% of your orders come through BNPL, that is around 480 dollars a month, or nearly 5,800 a year, in extra payment costs on this store.

That number on its own does not tell you whether BNPL is worth it. It tells you the price of admission. The mistake is treating payment fees as a fixed cost of doing business instead of a line item you manage like shipping or ad spend.

Two details make the real cost higher than the headline rate. First, when a customer returns a BNPL order, most providers do not refund your merchant fee. You wear the fee on revenue you never kept. In categories like fashion, where return rates of 20 to 30% are normal, that quietly compounds. Second, BNPL fees are charged on the GST-inclusive total, so the effective hit on your ex-GST revenue is higher than the sticker rate suggests.

If you have never broken payment costs out by method, start there. We covered the wider exercise in our payment processing audit, and it pairs with a proper contribution margin audit so you can see exactly which orders make you money.

One Year Into Regulation: What the June 2025 Rules Changed

BNPL stopped being the wild west on 10 June 2025. From that date, providers operating in Australia have needed an Australian Credit Licence, membership of the Australian Financial Complaints Authority, and compliance with modified responsible lending obligations under ASIC’s new framework. In practice that means Afterpay, Zip and the rest now run credit checks on new customers and assess spend limit increases properly.

A year on, here is what that has meant for store owners:

- Slightly more friction for first-time BNPL users. New customers face a credit check before approval, so the impulse “sign up at checkout and buy in 90 seconds” path has a speed bump. Expect marginally lower approval rates on brand-new BNPL accounts than you saw in 2024.

- A more stable provider landscape. Licensing costs pushed smaller players out, which is why your checkout decisions now realistically come down to Afterpay, Zip and PayPal Pay in 4.

- More trust at the top of the funnel. Regulated credit is easier to defend to customers, media and your own conscience. The sector growing 17.5% this year to a forecast US$18.34 billion in payments, according to ResearchAndMarkets, says regulation legitimised BNPL rather than killing it.

The takeaway: BNPL is now permanent retail infrastructure in Australia, not a fad. Which makes managing its cost properly even more important, because it is not going away on its own.

Where BNPL Genuinely Lifts Revenue

Fees are only half the equation. BNPL earns its place when it brings you orders and order value you would not have captured otherwise. The evidence worth knowing:

- Abandonment protection. PYMNTS’ 2025 research found 43% of consumers will walk away from a purchase without a BNPL option, and another 42% will trade down to a cheaper item. For stores selling to under-35s, the effect is stronger: 59% of Gen Y and 57% of Gen Z Australians used BNPL in the past six months, against just 15% of baby boomers.

- Order value uplift. Afterpay’s own merchant data claims AOV increases of 20 to 40%, concentrated in fashion and beauty. Treat vendor numbers with healthy scepticism, but the direction is consistent with what we see in member dashboards: BNPL orders routinely come in 15 to 30% above card orders on the same store.

- Directory traffic. Afterpay has around 3.5 million Australian users, and its shop directory and app send real referral traffic to listed stores. It is a discovery channel, not just a payment method.

Look at who uses it well. Princess Polly runs Afterpay alongside Shop Pay and Klarna, and makes the four-instalment price a visible part of the product page for a customer base that skews 18 to 25. Showpo does the same, with BNPL messaging woven into its sale events rather than bolted on. Both are fashion brands with AOVs in the 80 to 200 dollar band selling to young customers. That is the BNPL sweet spot.

A word on incrementality before you get excited about uplift numbers. A higher BNPL AOV does not automatically mean BNPL caused it. Customers who were always going to spend 200 dollars may simply prefer paying in instalments, which means you are paying premium fees on revenue you already had. The clean way to read it: compare your AOV and conversion before and after a placement change on your own store, not against a provider’s marketing deck. Your data beats their case studies every time.

Now invert it. If you sell 45 dollar consumables to customers in their 50s, BNPL is probably pure fee drag: the abandonment protection barely applies to your audience and the instalment maths on a small order motivates nobody. The point is not that BNPL is good or bad. It is that the answer is specific to your store, which is what the next section is for.

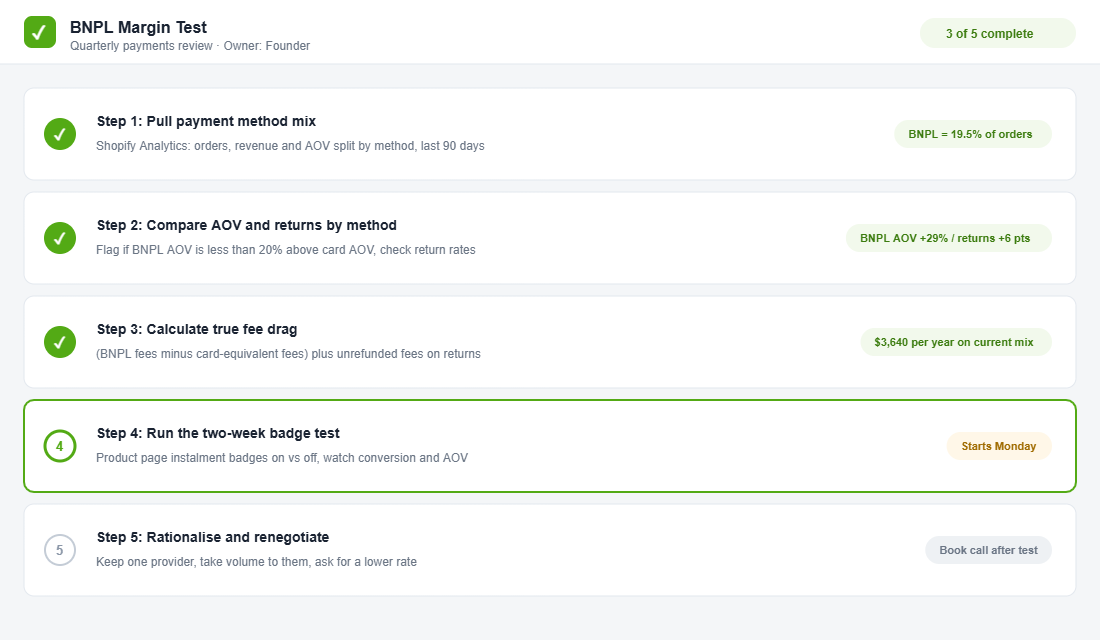

The BNPL Margin Test: A 5-Step Framework

This is the takeaway to actually run this week. One hour, five steps, and you will know whether BNPL is a profit lever or a leak on your store.

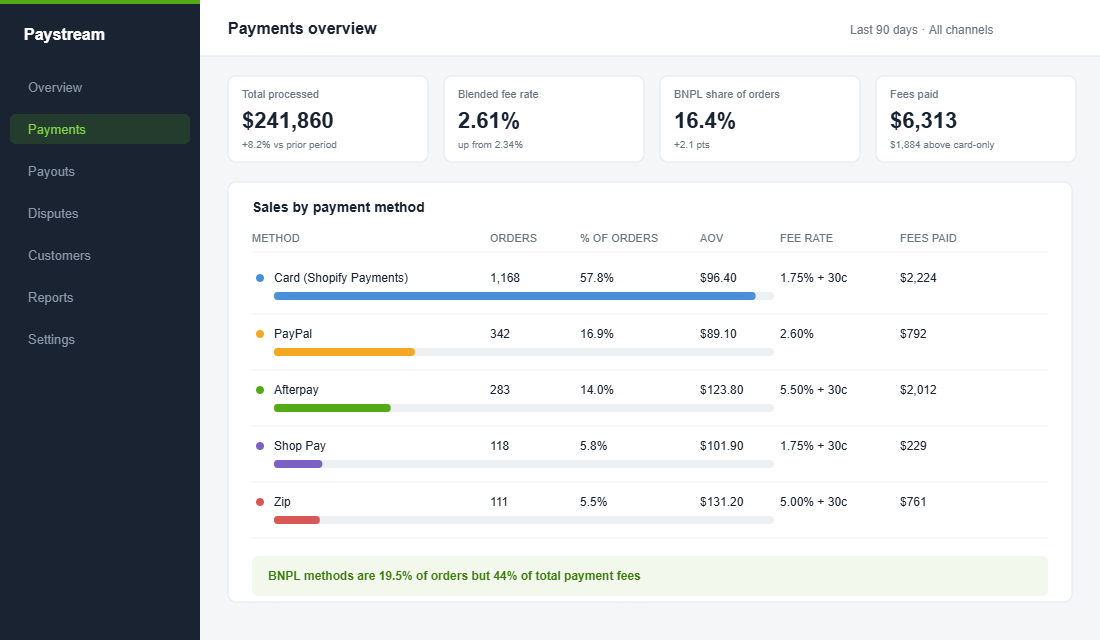

Step 1: Pull your payment method mix

In Shopify admin, go to Analytics, then Reports, and filter sales by payment method for the last 90 days. You want each method’s share of orders, share of revenue, and AOV. Most founders guess their BNPL share at 5% and find it is 15 to 20%.

Step 2: Compare AOV and return rates by method

If BNPL AOV is 20% or more above card AOV, the uplift story is real on your store. If BNPL AOV matches card AOV, you are paying triple fees for orders you would have won anyway. Check return rates by payment method too, because a high-return BNPL cohort is doubly expensive once you remember the fees are not refunded.

Step 3: Calculate the true fee drag

Multiply BNPL revenue by your blended BNPL rate, subtract what the same revenue would have cost through cards, and add the unrefunded fees on returned BNPL orders. That figure is your annual cost of offering instalments. Put it next to your contribution margin per order and you will know exactly how many incremental orders BNPL needs to bring you to break even.

Step 4: Test placement, not existence

Almost nobody should rip BNPL out of checkout cold. The smarter test is messaging placement: run two weeks with instalment badges on product pages versus two weeks with BNPL visible only at payment selection. If conversion holds when the badges come down, you can quietly de-emphasise BNPL and shift mix back towards cheaper methods without losing the safety net at checkout.

Step 5: Rationalise and renegotiate

Three BNPL providers at checkout adds choice paralysis, not conversion. Keep the one or two your customers actually use, then take your volume to the provider and ask for a better rate. Afterpay’s standard rates are negotiable once you are processing consistent monthly volume, and a drop from 5.5% to 4.5% on 15k of monthly BNPL revenue is 1,800 a year straight back into margin.

Setting It Up Properly on Shopify

If you have decided BNPL earns its place, set it up so you can measure it. Here is the clean setup:

- 1. Activate through Shopify Payments where possible. In Settings, then Payments, Shop Pay Installments and several BNPL wallets are managed natively. For Afterpay and Zip, add them under “Supported payment methods”, connect or create your merchant account, and confirm your settlement details.

- 2. Install the Afterpay On-Site Messaging app from the Shopify App Store. It renders the “4 payments of” line under your product price without you touching theme code. Configure it to show only above your minimum threshold (for example, orders over 50 dollars) so you are not advertising instalments on items where they add nothing.

- 3. Mirror the setup for Zip with the Zip widget if your audience uses it, but resist running more than two BNPL badges on a product page. Visual clutter costs more conversions than a missing logo does.

- 4. Build a payment-method report. In Shopify Analytics, save a custom report of sales by payment method, monthly. This is the dashboard the Margin Test runs off, and it takes ten minutes once.

While you are in there, it is worth running our 7-point checkout audit. BNPL decisions sit inside a wider checkout system, and a slow or cluttered checkout will cost you more than any payment fee.

Badge Placement: Where BNPL Messaging Helps and Where It Hurts

BNPL messaging is merchandising, and like all merchandising it has good and bad placements.

- Product page, under the price: the highest-value placement for orders between roughly 80 and 300 dollars. “4 payments of 45” reframes a 180 dollar purchase into a weekly coffee budget decision.

- Cart drawer: useful as a nudge when cart values climb above your card-order AOV. Keep it to one line.

- Homepage banners: almost always wasted space. Nobody arrives at your store because of your payment options; give the slot to product or offer.

- Low-priced items: hide instalment messaging below 50 dollars. Four payments of 7 dollars reads as desperate and adds visual noise to your product page for zero lift.

Treat each placement as a test, not furniture. The two-week badge experiment from Step 4 of the Margin Test will tell you more about your store than any benchmark, ours included.

Can You Pass the Fees On? The Surcharge Question

The obvious founder instinct is to surcharge. If Afterpay costs you 5%, why not add 5% for customers who choose it, the way many businesses do with American Express?

Because your merchant agreement almost certainly forbids it. Afterpay and Zip both include no-surcharge clauses in their standard Australian merchant terms, and unlike card schemes, BNPL providers are not currently forced to allow surcharging. The RBA has flagged the inconsistency more than once, but as of mid-2026 the contractual position stands: surcharge a BNPL order and you are in breach, which can get your facility terminated.

So the fee has to be managed inside your pricing, not bolted onto it. Three legitimate levers:

- Price for your blended payment cost. Work out your weighted average fee across all methods and treat that number, not the card rate, as your payments line when you set prices and plan promotions.

- Set a BNPL-aware free shipping threshold. If instalment orders cluster just under your threshold, a small lift can push BNPL customers to add an item, recovering fee in extra contribution. Our free shipping threshold playbook walks through the maths.

- Steer with defaults, not penalties. You cannot punish BNPL use, but you can present cheaper methods first, keep express wallets like Shop Pay prominent, and let BNPL sit one tap deeper for the customers who actually want it.

Which Provider Fits Which Store

If the Margin Test says BNPL stays, the last decision is which logo earns the slot. The honest answer for most Aussie Shopify stores:

- Afterpay if your customers skew female and under 35, especially in fashion, beauty and lifestyle. With roughly 38% of Australians having used it, per Finder, it is the default instalment brand in this country, and its shop directory still sends meaningful referral traffic to listed stores.

- Zip if your AOV regularly clears 300 dollars. Zip Pay handles everyday amounts, while Zip Money extends to larger purchases with longer terms, which suits furniture, fitness equipment and electronics far better than a four-instalment product does.

- PayPal Pay in 4 as a low-effort second option if you already offer PayPal, since it rides on your existing PayPal rates rather than a separate BNPL agreement. For some stores that makes it the cheapest instalment option on the page.

- Shop Pay Installments is worth watching as Shopify expands it in Australia, because native checkout integration plus Shop App distribution is a strong combination. Check current availability for Australian merchants before you plan around it.

One primary BNPL provider, chosen to match your customer and your AOV band, nearly always beats three logos fighting for the same tap.

How the Pieces Compound

Run the system end to end and the individual moves stack. Say you are doing 80k a month with 18% of revenue through BNPL at a blended 5.5%.

Rationalising from three providers to one tidies your checkout and bumps conversion a touch. Negotiating that provider down to 4.5% saves around 1,700 a year on its own. Hiding instalment badges on sub-50 dollar items shifts a slice of small orders back to cards, saving another grand or so. Keeping the badges prominent on your 150 dollar hero products protects the AOV uplift where it is real. None of these is dramatic. Together they are typically 4,000 to 6,000 a year back into a store this size, for one afternoon of work and a two-week test. That is the difference between treating payments as plumbing and treating them as a profit lever.

The founders who win this game are not the ones with the strongest opinions about Afterpay. They are the ones who know their payment-method mix cold, test placements like they test ad creative, and renegotiate rates every twelve months. BNPL is neither saint nor villain. It is a tool with a price tag, and now you know how to read it.

Inside eCommerce Circle, payment economics sits in the Profit pillar we work through with every member. If you want a second opinion on whether BNPL is earning its keep on your store, let’s talk.